The Complete Valuation Playbook for Civil Engineering Businesses

A practical breakdown of how civil engineering businesses are valued and what drives high multiples

Civil engineering businesses are rarely valued on revenue alone. Buyers look at what kind of work you do, how predictable your backlog is, how much risk sits inside your contracts, how much working capital the business consumes, and whether your team can keep winning and delivering projects after a sale.

Now is an important time to think about valuation because infrastructure spending, grid investment, transport upgrades, water systems, renewables, housing delivery, and public works are all creating buyer interest. But that does not mean every contractor gets a premium multiple. The data shows a clear split: ordinary project-based civil contracting is valued cautiously, while specialist, high-margin, mission-critical infrastructure capability can attract much stronger buyer interest.

This playbook shows what civil engineering businesses actually sell for, what public markets suggest, what pushes valuation up or down, and how you can assess your own business before a sale in the next 1-12 months.

1. What Makes Civil Engineering Unique

Civil engineering is a broad sector. A founder running a groundworks contractor is not valued the same way as a specialist high-voltage utility contractor, a rail infrastructure business, a piling and foundations specialist, or an engineering consultancy.

The main types of businesses in this market usually include:

The sector has several valuation features that make it different from simpler businesses. Revenue can be large, but margins are often thin. A company can be busy, well known, and still not generate much free cash if projects require equipment, bonding, labor, materials, and working capital before cash is collected.

Buyers also worry about project risk. One poorly priced contract, one dispute, or one safety incident can damage a year of profit. That is why buyers spend so much time checking contract terms, change order recovery, customer concentration, claims history, safety record, equipment condition, backlog quality, and whether management is strong enough to run the business without the founder.

Civil engineering also has a people problem and a people opportunity. Skilled labor, project managers, estimators, engineers, foremen, and safety leaders are hard to replace. A company with a trained, loyal workforce and a second layer of management is worth more than a founder-led business where all relationships and decisions sit with one person.

2. What Buyers Look For in a Civil Engineering Business

Buyers start with the basics: size, growth, margins, cash flow, backlog, customer mix, and management depth. But in civil engineering, those basics are not enough. A buyer also wants to know whether the revenue is high-quality or just high-volume.

A USD 100m revenue contractor with weak margins and heavy project risk may be less attractive than a USD 25m specialist business with repeat customers, strong margins, and scarce technical capability. The transaction data supports this. Scale alone did not guarantee a premium valuation. Differentiated capability, specialist end markets, and proven profitability mattered more.

Buyers usually care about:

Strategic buyers usually ask, “What does this business help us do that we cannot already do?” That may mean entering a new region, gaining utility credentials, adding rail or power expertise, acquiring a trained workforce, improving project delivery, or winning larger tenders.

Private equity buyers think slightly differently. They ask whether they can buy the business at a reasonable entry price, improve it, grow it, and later sell it to a larger buyer at a better valuation. They care about who might buy the business in 3-7 years, whether it can become a platform for further acquisitions, and whether the company has enough systems and leadership to scale.

In simple terms, private equity wants a business that is not just profitable today, but buildable. That means clean numbers, repeatable estimating, strong project controls, a clear market niche, and a management team that can absorb growth without breaking operations.

3. Deep Dive: Why Specialist Capability Beats General Contracting

The most important valuation nuance in civil engineering is this: buyers do not pay premium multiples just because a company is in infrastructure. They pay premium multiples when the business owns a scarce capability in an attractive infrastructure theme.

The data shows this clearly. Some large civil engineering and heavy infrastructure businesses traded at low revenue multiples because their work was broad, competitive, or low-margin. By contrast, businesses with specialist technical niches, high-margin consulting models, or exposure to structurally growing infrastructure themes achieved stronger outcomes.

This matters because “civil engineering” can mean very different things. A contractor doing general groundworks for developers may face tender pressure, labor cost inflation, weather delays, and working capital swings. A specialist in high-voltage transmission, rail systems, complex bridges, grid connections, or engineering consulting may have fewer direct substitutes and stronger buyer demand.

Buyers pay more when they believe the business gives them access to something hard to build quickly. That could be qualified labor, certifications, public-sector approvals, technical reputation, equipment fleet, long-term framework agreements, or trusted relationships with utilities and transport authorities.

If your business looks more like a general contractor today, that does not mean you are stuck at the low end. Over 6-12 months, you can improve the way buyers see your business by separating specialist work from commodity work, showing margin by project type, highlighting repeat customers, documenting technical credentials, and building a stronger case around backlog quality.

The goal is not to pretend your business is something it is not. The goal is to show buyers exactly where the quality sits inside the company. Often the premium part of the business is already there, but it is buried inside messy reporting.

4. What Civil Engineering Businesses Sell For - and What Public Markets Show

The valuation data points to a wide range. That is normal in civil engineering because the sector includes everything from low-margin contractors to specialist consultants and mission-critical infrastructure service providers.

For founders, the key lesson is simple: do not anchor on the highest multiple in the market. Instead, identify which group your business actually resembles, then ask what would move it higher or lower within that group.

4.1 Private Market Deals Similar Acquisitions

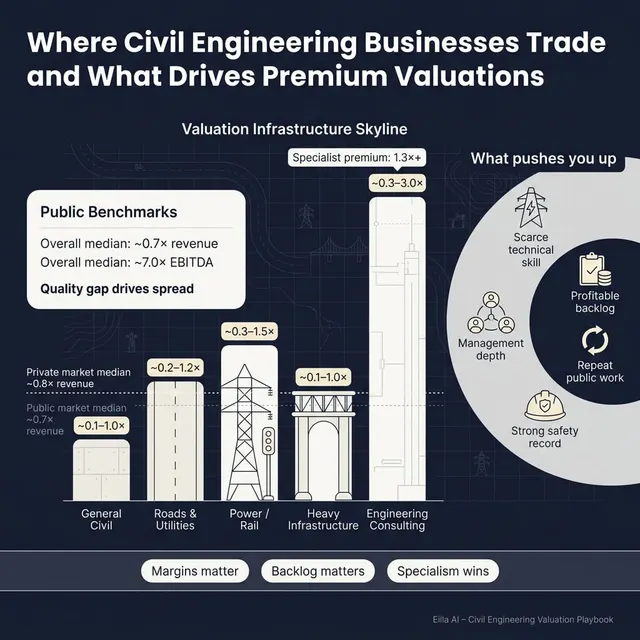

The private transaction data shows an overall average EV/Revenue multiple of about 0.8x and a median of about 0.8x. On EBITDA, the average was about 6.4x and the median was about 6.2x.

But the spread is wide. Some heavy civil and infrastructure contractors traded around 0.1x-1.0x revenue, while specialist utility, rail, power, and consulting-led businesses could command stronger valuation logic when margins, technical capability, and strategic fit were clear.

These ranges are illustrative. A private company with USD 10m of revenue, low margins, and customer concentration will not be valued the same as a specialist contractor with repeat customers, strong margins, and scarce technical credentials.

The most important pattern is that large revenue did not always create a high valuation. Some very large civil contractors traded at low revenue multiples because margins were thin or the business looked project-based and competitive. Meanwhile, smaller specialist or consulting-led firms achieved better outcomes because buyers were paying for quality, not just size.

4.2 Public Companies

Public markets provide a useful reference point, but not a direct price tag for your company. Public companies are usually larger, more diversified, more liquid, and easier for investors to buy and sell. A private founder-owned business usually receives a discount unless it has something strategically scarce.

The public company data shows an overall average EV/Revenue multiple of about 1.7x and a median of about 0.7x. On EBITDA, the average was about 12.3x and the median was about 7.0x. These multiples are best understood as a mid to end of 2025 market reference point.

The public data also contains outliers. Some companies show very high revenue or EBITDA multiples because of special circumstances, unusual margins, regional market factors, low EBITDA bases, or investor expectations. Founders should not treat those outliers as normal private-company valuation benchmarks.

A practical way to use public multiples is as a reference band. If your business is smaller, private, regional, project-based, and founder-dependent, buyers will usually apply a discount to public multiples. If your business has scarce technical capability, strong margins, recurring public-sector frameworks, and a deep management team, it may move closer to the stronger end of the range.

5. What Drives High Valuations Premium Valuation Drivers

Premium valuations in civil engineering come from reducing buyer risk and increasing strategic value. The best-positioned businesses make buyers feel that they are acquiring something difficult to replicate.

Differentiated capability, not just revenue scale

The data shows that scale alone is not enough. Large contractors can still trade at modest valuations if their work is low-margin, competitive, or hard to differentiate.

Buyers pay more when your company has a capability that competitors cannot easily copy. Examples include complex bridge engineering, high-voltage power line work, rail systems, tunneling, deep foundations, utility connections, water infrastructure, or specialist project management.

For a founder, the practical point is this: show buyers where your business is truly different. Separate specialist revenue from commodity revenue. Show margins by work type. Make the case that your best work is not easily replaceable.

Exposure to long-term infrastructure themes

Premium outcomes are more likely when the buyer sees your business as a platform into a growing market. In civil engineering, that can include grid expansion, renewable energy infrastructure, water and sewer upgrades, rail modernization, transport infrastructure, and public-sector resilience projects.

Buyers care because these themes are backed by long-term spending needs. A company with credible access to those markets may be more valuable than one that depends mostly on short-term private developer activity.

Practical examples include framework agreements with utilities, recurring work for transport authorities, specialist power infrastructure teams, or a track record in public infrastructure programs.

Strategic fit with the acquirer

A buyer may pay more if your company helps them expand geographically, win larger contracts, cross-sell services, add skilled labor, improve delivery capability, or enter a market they have targeted.

This is why valuation is not only about your standalone financials. The same business may be worth more to one buyer than another because it unlocks a specific strategic plan.

Your job before a sale is to identify these buyer-specific angles. For one buyer, your value may be regional access. For another, it may be utility credentials. For another, it may be workforce, equipment, customer relationships, or public-sector approvals.

Management continuity

Civil engineering businesses are people-led. Buyers worry that customers, estimators, project managers, and site supervisors will leave after closing.

A strong second layer of management can protect valuation. So can clear succession planning, retained leaders, documented customer relationships, and incentive plans that keep key people engaged.

This does not mean you have to stay forever. It means buyers need confidence that the business can keep winning and delivering work when ownership changes.

Specialist labor and mission-critical work

Scarce labor is a major valuation driver. Businesses with trained crews, certified engineers, safety-sensitive utility teams, high-voltage specialists, rail workers, or experienced project managers can become very attractive to buyers.

The more mission-critical the work, the better. Power, water, rail, bridges, roads, drainage, and utilities are not optional services. If your business supports essential infrastructure and has the credentials to do work safely, buyers will take that seriously.

High-margin, asset-light models

Consulting, project management, engineering design, and supervision businesses often attract stronger valuation logic than equipment-heavy contracting businesses. They usually require less capital, carry less project execution risk, and can produce stronger margins.

That does not mean contractors cannot achieve good valuations. But if part of your business is advisory, design, engineering, program management, or specialist inspection, make sure buyers can see it clearly.

Clean financials and predictable performance

Buyers pay more when they trust the numbers. Clean financials, clear project margin reporting, accurate backlog, sensible revenue recognition, and consistent EBITDA all reduce uncertainty.

In civil engineering, buyers also care about claims, change orders, retentions, bonding, equipment debt, and working capital. If those are messy, buyers will either lower the price or ask for more protection in the deal structure.

6. Discount Drivers What Lowers Multiples

Discount drivers are not always fatal. Many can be improved before a sale. But if buyers discover them late in the process, they often reduce valuation quickly.

The biggest discount driver is weak or unstable margins. Civil engineering buyers know revenue can look impressive while profit remains thin. If your projects regularly miss budget, if change orders are poorly recovered, or if profit depends on one or two exceptional jobs, buyers will be cautious.

Another major issue is customer concentration. If a large share of revenue comes from one developer, municipality, utility, or prime contractor, buyers will worry about what happens if that relationship changes. Long relationships help, but they do not fully remove concentration risk.

Project-based revenue also lowers valuation when backlog is short or low quality. Buyers want to know what revenue is already secured, how profitable it is expected to be, and how much is still subject to risk.

Other common discount drivers include:

In this sector, buyers are also careful with bonding capacity, insurance claims, environmental exposure, subcontractor quality, and compliance with public-sector procurement rules. Any weakness in these areas can lead to a lower multiple, more seller financing, a larger escrow, or an earnout tied to future performance.

7. Valuation Example: A Civil Engineering Company

This example is fictional and designed only to show valuation logic. It is not investment advice, not a formal valuation, and not a fairness opinion.

Assume a fictional company called HarborPoint Civil Works. It has USD 10m of revenue and operates as a regional civil engineering and groundworks contractor. It serves housebuilders, local authorities, and commercial developers. Its work includes site preparation, drainage, small roadworks, substructures, and public realm projects.

HarborPoint has been operating for decades, has a loyal workforce, and has a decent local reputation. But it is still mostly a traditional contractor. It is not a software business, not a high-margin consultancy, and not a scarce national infrastructure platform.

The valuation logic would work like this:

First, we compare HarborPoint to relevant private civil engineering and infrastructure transactions, where many contractor-type businesses fall around 0.1x-1.0x revenue, with the overall private transaction median around 0.8x revenue and about 6.2x EBITDA.

Second, we compare it to public market reference points. Public civil engineering and infrastructure companies show a wide range, but the overall public median EV/Revenue is about 0.7x and median EV/EBITDA is about 7.0x. Since HarborPoint is private, smaller, regional, and more founder-dependent, it would normally trade at a discount to stronger public companies.

Third, we adjust for company quality. If HarborPoint has strong margins, repeat customers, clean backlog, and a capable management team, it can sit toward the higher end. If margins are weak, backlog is uncertain, or financial reporting is messy, it moves lower.

For a traditional civil engineering contractor like HarborPoint, a USD 6m-10m enterprise value, or 0.6x-1.0x revenue, is a defensible core range if the company has normal contractor margins, reasonable backlog, and no major red flags.

A stronger outcome may be possible if HarborPoint has a clearer specialty, such as utility infrastructure, frameworks with public agencies, stronger EBITDA margins, low customer concentration, and a management team that can run the business without the founder.

A lower outcome is also possible. If the company has weak margins, disputed projects, poor financial reporting, heavy working capital needs, or high dependence on one customer, buyers may push the valuation below the core range.

The lesson for founders is that two civil engineering companies with the same USD 10m revenue can be worth very different amounts. Revenue starts the conversation. Margin quality, risk, backlog, specialization, and buyer fit determine where the conversation ends.

8. Where Your Business Might Fit Self-Assessment Framework

Use this as a simple self-check before going to market. Score each factor from 0 to 2.

A score of 0 means it is a weakness. A score of 1 means it is acceptable but not special. A score of 2 means it is a clear strength that a buyer would notice.

How to interpret your score

If you score mostly 2s in the high-impact category, you are closer to the upper end of the relevant valuation range. Buyers will still test the details, but your business likely has the ingredients of a stronger process.

If you score mostly 1s, you may be in the fair-market middle. That is not bad. It means the business is saleable, but the valuation will depend heavily on buyer appetite, process quality, and how well the story is presented.

If you score several 0s, you may want to fix issues before launching a sale. The goal is not perfection. The goal is to remove obvious reasons for buyers to discount the business.

A useful exercise is to ask: “Which three improvements would most change how a buyer sees us?” In civil engineering, the answer is often project margin reporting, backlog quality, management depth, and customer diversification.

9. Common Mistakes That Could Reduce Valuation

The first mistake is rushing the sale. A civil engineering business needs preparation before going to market. Buyers will ask for project-level margins, backlog schedules, customer history, equipment records, safety data, working capital details, and contract summaries. If those are not ready, buyers assume risk.

The second mistake is hiding problems. Issues will surface during diligence. A disputed contract, weak margin project, customer loss, safety incident, or overdue receivable is better handled with a clear explanation than discovered late by the buyer. Hiding problems destroys trust and usually lowers value more than the problem itself.

The third mistake is weak financial records. Many founders know their business well but do not have financial reporting that proves the story. In civil engineering, buyers need to see revenue by project type, gross margin by job, change order recovery, retention balances, equipment costs, overhead allocation, and backlog profitability. Improving this over 6-12 months can materially improve buyer confidence.

The fourth mistake is not running a structured, competitive sale process. Research and market experience consistently show that using an advisor to run a competitive process can lead to meaningfully higher purchase prices, often around 25% higher than a less structured approach. The reason is simple: competition creates price discovery.

The fifth mistake is revealing the price you want too early. If you tell buyers you are looking for USD 10m of enterprise value, many will anchor around that number and offer USD 10.1m or USD 10.2m. You may never find out that another buyer would have paid more. Let the market come back with offers.

A sector-specific mistake is failing to explain project risk properly. If you present all backlog as equal, buyers will not believe it. Break it down by signed work, expected start date, gross margin, customer, contract type, and delivery risk.

Another mistake is not separating commodity work from specialist work. If 30% of your revenue comes from high-value utility, rail, drainage, or geotechnical projects, but you report everything as one blended contractor business, you may lose the chance to tell a stronger valuation story.

10. What Civil Engineering Founders Can Do in 6-12 Months to Increase Valuation

Improve the numbers buyers trust

Start with project-level margin reporting. Buyers need to see which projects make money and why. Break out revenue, direct labor, materials, subcontractors, equipment costs, change orders, and gross margin by project type.

Clean up working capital. Prepare aging schedules for receivables, payables, retentions, claims, and work-in-progress. Buyers dislike surprises in cash conversion, especially in construction.

Review underperforming projects before going to market. A bad project is easier to explain if you can show it was isolated, completed, and not representative of current bidding discipline.

Strengthen backlog and contract visibility

Build a clean backlog schedule. Include customer name, project type, contract value, expected revenue timing, expected margin, signed status, and main risks.

Highlight repeat customers and frameworks. If a local authority, utility, developer, or prime contractor has used you repeatedly, show the history clearly. Repeat work helps buyers believe revenue can continue.

Separate secured work from pipeline. Buyers will give more credit to signed backlog than informal opportunities. Do not overstate pipeline quality.

Make the business less founder-dependent

Identify who owns estimating, operations, customer relationships, finance, safety, and project delivery. If everything points back to you, buyers will discount the business.

Develop a management continuity plan. This may include retention bonuses, role clarity, employment agreements, or equity rollover for key leaders.

Document key customer relationships. Buyers do not just want names in a spreadsheet. They want to know who talks to whom, how often, and why the customer keeps coming back.

Show your specialist edge

If you have specialist credentials, make them visible. This may include utility approvals, safety certifications, rail qualifications, public-sector registrations, specialist equipment, technical staff, or difficult project references.

Break out higher-value work. If utility, power, rail, drainage, geotechnical, or public infrastructure work has better margins or stronger demand, show it separately.

Create case studies for complex projects. Buyers pay more when they understand what you can do that others cannot easily replicate.

Reduce diligence friction

Prepare a clean data room before launching a process. Include financial statements, management accounts, project margin schedules, backlog, customer data, employee information, equipment lists, insurance, safety records, contracts, and legal documents.

Fix obvious accounting issues. Revenue recognition, cost accruals, related-party expenses, equipment leases, and owner add-backs should be clear before buyers review the business.

Get your story straight. A good sale narrative should explain what you do, why customers choose you, where growth will come from, and why the business can thrive after ownership changes.

11. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor can help you reach more relevant buyers, faster. In civil engineering, the best buyer may not be the obvious local competitor. It could be a strategic acquirer looking for utility capability, a larger contractor expanding into your region, a private equity-backed infrastructure platform, or an international group seeking specialist talent.

AI can expand the buyer universe to hundreds of qualified acquirers based on deal history, strategic fit, financial capacity, geography, end-market exposure, and likely synergies. More relevant buyers means more competition, stronger offers, and a higher chance the deal closes even if one buyer drops out.

AI also helps accelerate the early stages of a process. Buyer matching, outreach preparation, marketing materials, and diligence support can move faster than a manual-only process. That can help founders reach initial conversations and offers in under 6 weeks, while still keeping the process structured.

The best outcomes still require expert human judgment. Experienced M&A advisors help frame the business, prepare credible materials, manage buyer tension, negotiate terms, and protect value during diligence. AI enhances that work by improving speed, coverage, and insight. The result is Wall Street-grade advisory quality without traditional bulge bracket costs.

If you'd like to understand how our AI-native process can support your exit - book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.