The Complete Valuation Playbook for Compliance and Certification Services Businesses

A practical breakdown of how compliance and certification services businesses are valued and what drives higher multiples.

If you own a compliance, certification, testing, assurance, regulatory training, or technical compliance services business, valuation is not just about revenue size. Buyers care about what type of compliance problem you solve, how recurring the revenue is, how regulated your customers are, and whether your expertise can scale beyond founder-led delivery.

This matters now because compliance markets are being reshaped by consolidation, rising regulation, supply chain scrutiny, sustainability requirements, and buyer demand for trusted assurance providers. Larger testing, inspection, certification, software, training, and consulting platforms are actively looking for businesses that can deepen their vertical expertise or expand their geographic reach.

This playbook explains what businesses in this sector actually sell for, what pushes valuations up or down, how to think about public market multiples, and what you can do in the next 6-12 months to improve your position before a sale.

1. What Makes Compliance and Certification Services Unique

Compliance and certification services sit at the intersection of regulation, trust, and operational risk. Your customer is often not buying a “nice to have” service. They are buying the right to operate, sell into a market, pass an audit, meet a customer requirement, or reduce the risk of regulatory failure.

That is why this sector often attracts buyer interest even when broader markets are uncertain. Regulation does not disappear in a downturn. Product safety rules, workplace health and safety obligations, environmental standards, pharmaceutical validation requirements, quality assurance needs, and certification obligations continue.

The sector includes several types of businesses:

The main valuation question is: are you a labor-heavy services business, a trusted recurring certification platform, or a software-enabled compliance workflow?

That distinction matters. In the source data, traditional consulting and services-led compliance businesses generally transact at lower revenue multiples than software-enabled regulatory intelligence or compliance management systems. Buyers pay more when compliance demand is recurring, embedded, technical, and difficult to replace.

Key risks buyers will always check include auditor capacity, customer concentration, accreditation status, regulatory exposure, quality of records, employee dependence, claims history, and whether revenue would continue if the founder stepped back.

2. What Buyers Look For in a Compliance and Certification Services Business

Buyers start with the basics: revenue scale, growth, profitability, customer retention, and clean financial records. But in this sector, those are only the first layer.

They also want to know whether your services are mission-critical. A company that helps customers maintain legally required certification, pass regulatory inspections, or sell into tightly controlled industries is usually more attractive than a general advisory firm that performs one-off projects.

Buyers also care about how repeatable the revenue is. Annual certification renewals, recurring audits, subscription-based compliance monitoring, retained training programs, and multi-year validation support are easier to underwrite than project-by-project consulting.

Industry-specific questions buyers will ask include:

Strategic buyers often look for fit. They may want a new geography, a new technical niche, a stronger auditor network, a foothold in life sciences, clean energy, construction, product safety, environmental compliance, workplace safety, or regulated manufacturing.

Private equity buyers think slightly differently. They ask: “Can we buy this business today, improve it, and sell it for more in 3-7 years?” They consider the entry multiple, the likely exit multiple, and the levers they can pull. Those levers might include better pricing, cross-selling services, adding software, acquiring smaller competitors, improving utilization, professionalizing sales, or expanding into adjacent regulated markets.

A private equity buyer will also think about the next buyer. Could a global testing, inspection, and certification platform buy the business later? Could a larger compliance software platform value the customer base? Could another private equity fund pay more once the company is bigger and more professionalized? That future buyer logic shapes what they are willing to pay today.

3. Deep Dive: Services-Led Compliance vs Software-Enabled Compliance

One of the biggest valuation questions in this sector is whether your business behaves like a traditional services business or a software-enabled compliance platform.

This is not about whether you use technology internally. Almost every serious compliance business does. The real question is whether technology changes the economics of the business. Does it make revenue more recurring? Does it reduce delivery cost? Does it increase switching costs? Does it help customers monitor compliance continuously rather than buying advice only when a problem appears?

The source data shows a clear pattern. Compliance preparation and management systems software traded at meaningfully higher revenue and EBITDA multiples than traditional consulting-led businesses. By contrast, metrology, environmental consulting, safety engineering, and technical compliance consulting businesses generally traded at lower multiples, even when they were profitable.

Buyers understand why. A pure services business usually grows by adding people. More audits, more projects, and more consulting work require more expert hours. That can be a very good business, but it is harder to scale quickly.

A software-enabled compliance business can grow differently. Once the platform is built, each additional customer may require less incremental delivery effort. Customers may also stay longer because the software becomes part of their daily compliance workflow.

If your business is services-led today, that does not mean you need to become a software company in the next year. But you can move in the right direction. Package repeatable services. Standardize audit workflows. Build customer portals. Track renewal revenue. Create subscription-style compliance monitoring. Turn expert knowledge into templates, content, data, and repeatable processes.

Buyers do not pay premium multiples for technology buzzwords. They pay when technology improves retention, margins, growth, and customer dependence.

4. What Compliance and Certification Services Businesses Sell For - and What Public Markets Show

The data shows a wide valuation range across the sector. That is normal. “Compliance and certification services” includes global testing platforms, laboratory networks, regulatory software, training providers, asset compliance specialists, and traditional consulting firms.

The right comparison depends on your business model. A certification platform with recurring audits should not be valued like a one-off consulting firm. A regulatory software company should not be valued like an equipment-heavy testing provider. A niche technical compliance business serving regulated global customers may deserve a different view from a local advisory practice.

4.1 Private Market Deals Similar Acquisitions

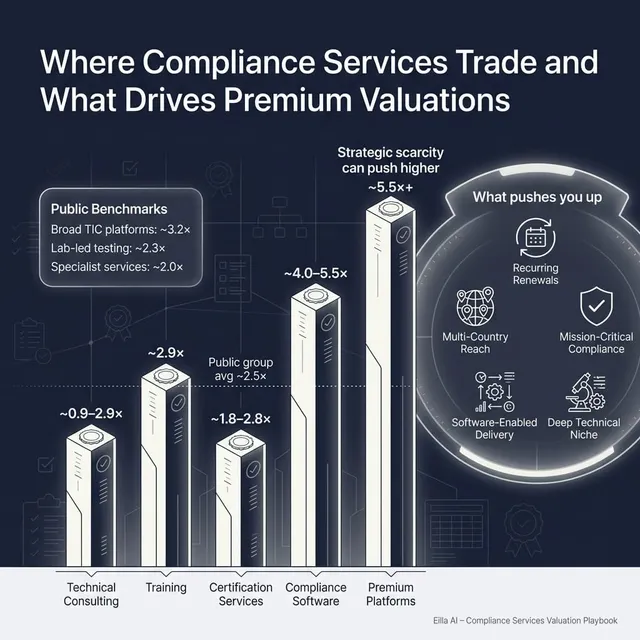

In the precedent transaction data, the overall private deal average was around 3.3x EV/Revenue, with a median of around 2.9x. That headline number hides major differences by segment.

Compliance, certification preparation, and management systems software showed the strongest valuation profile, with average EV/Revenue of around 4.6x and median EV/Revenue of around 5.4x. The available EBITDA multiple for this group was around 20.8x, which is high and reflects software-like characteristics.

Quality, safety, environmental, and technical compliance consulting services were more moderate. This group averaged around 2.5x EV/Revenue, with a median of around 2.4x. Where EBITDA multiples were available, the average and median were around 4.9x, reflecting a more services-heavy model.

Health, safety, and compliance training showed around 2.9x EV/Revenue in the source data. Training can be attractive when it has recognized credentials, repeat customers, digital content, and strong margins. But it still depends heavily on growth, brand, and delivery model.

These ranges are illustrative. A fast-growing, high-margin, recurring compliance platform can trade above the sector average. A small, local, founder-dependent consulting practice with weak financial records can trade below it.

4.2 Public Companies

Public companies provide useful reference points, but they are not direct price tags for private businesses. Public companies are larger, more diversified, more liquid, and often more professionally managed. Buyers usually apply a discount when comparing smaller private companies to listed groups.

As of the mid to end of 2025 data set, the overall public company group traded at an average EV/Revenue of around 2.5x and a median EV/Revenue of around 2.5x. Average EV/EBITDA was around 13.3x, with a median of around 12.3x.

Broad-based testing, inspection, certification, and assurance platforms traded higher than the overall set on revenue, with average EV/Revenue of around 3.2x and average EV/EBITDA of around 14.1x. These businesses benefit from scale, brand trust, global networks, and broad customer coverage.

Laboratory-led analytical testing and scientific services traded at around 2.3x average EV/Revenue and around 12.7x average EV/EBITDA. Specialist technical testing and sector-focused certification services traded at around 2.0x average EV/Revenue and around 13.3x average EV/EBITDA.

Founders should use public multiples as a valuation compass, not a guaranteed outcome. A smaller private business will usually be adjusted down for lower scale, customer concentration, lower liquidity, and higher key-person risk.

But there are exceptions. A scarce asset with a regulated niche, strong recurring revenue, clean financials, high margins, international relevance, and strategic importance to a buyer can command a premium even if it is smaller.

5. What Drives High Valuations Premium Valuation Drivers

High valuations in compliance and certification services usually come from a combination of mission-critical demand, repeatable revenue, defensible expertise, and scalable delivery.

5.1 Regulated, Mission-Critical End Markets

Buyers pay more when customers must buy your service to operate, sell, comply, or pass inspection. This includes life sciences, healthcare, medical devices, aerospace, clean energy, food safety, construction materials, regulated manufacturing, environmental compliance, and workplace safety.

The reason is simple: these budgets are harder to cut. A customer may delay marketing spend, but they cannot easily ignore required certification, validation, or compliance monitoring.

A premium business is not merely “in compliance.” It is embedded in the customer’s compliance workflow. It helps the customer stay audit-ready, maintain certification, meet regulatory obligations, or access a market.

5.2 Recurring Revenue and Customer Stickiness

Recurring certification renewals, ongoing audit programs, retained compliance monitoring, repeat training, and subscription-style software support higher valuations.

Buyers care because recurring revenue makes next year easier to predict. If a large share of revenue repeats automatically or semi-automatically, the buyer takes less risk.

Practical examples include annual recertification cycles, multi-year customer contracts, recurring regulatory monitoring subscriptions, customer portals that store compliance history, and training programs that refresh credentials each year.

5.3 Deep Technical Specialization

Generic consulting is easier to replace. Deep technical expertise is not.

Premium outcomes are more likely when the business serves a technically complex niche, such as life sciences validation, software as a medical device, global regulatory monitoring, calibration and quality systems in regulated facilities, renewable energy supply chain assurance, or specialized construction material certification.

Specialization matters most when it creates pricing power. A niche is valuable when customers see you as one of the few credible providers, not just one of many consultants.

5.4 Software-Enabled Workflows

Regulatory software and tech-enabled compliance workflows tend to receive stronger buyer interest than traditional people-heavy services.

This does not mean every founder should suddenly call the business a software company. Buyers will test the claim. They will look at subscription revenue, gross margin, customer usage, renewal rates, product roadmap, and whether the platform reduces manual delivery.

The strongest story is: “Our expertise is delivered through a repeatable system that customers use regularly, and each new customer can be served without adding the same amount of headcount.”

5.5 Geographic Reach and Multinational Relevance

Compliance becomes more valuable when it helps customers operate across borders. Regulations differ by country. Standards differ by industry. Audit and certification requirements become more complex for multinational customers.

Buyers may pay more for a business that already serves customers across regions, has an international auditor network, supports multi-country regulations, or can be plugged into a larger global platform.

Geographic reach is not valuable just because a website says “global.” Buyers want evidence: revenue by country, customer locations, delivery capability, partner networks, language coverage, and retention across regions.

5.6 High Margins and Scalable Delivery

High-margin, asset-light delivery models are attractive because more revenue can turn into profit and cash flow.

In this sector, strong margins often come from standardized delivery, credentialed training content, software tools, repeatable audit processes, efficient utilization, and pricing power in technical niches.

A business that needs to hire a senior expert for every new dollar of revenue will usually receive a lower multiple than one that can scale through systems, templates, content, technology, and a trained delivery bench.

5.7 Clean Financials and Strong Management

Clean financials are not glamorous, but they matter. Buyers pay more when they trust the numbers.

That means clear revenue recognition, proper separation of one-time and recurring revenue, customer-level margin reporting, accurate backlog, clean working capital records, and documented adjustments.

A strong leadership bench also matters. If the founder is still the main salesperson, technical expert, customer relationship owner, and problem solver, buyers will worry about what happens after closing.

6. Discount Drivers What Lowers Multiples

Lower valuations usually come from risk, uncertainty, or lack of scalability.

The source data shows that businesses which are more local, equipment-heavy, consulting-led, or people-intensive tend to transact at lower multiples than software-enabled and recurring compliance platforms.

The most common discount drivers include:

Negative EBITDA is a major issue. A compliance business can still be valuable if it is growing quickly or building software, but buyers will ask why it is losing money. Is it investing for growth, or is the delivery model structurally unprofitable?

Services-heavy businesses can also be discounted if growth requires linear headcount additions. If revenue growth always requires adding more senior consultants, auditors, or technical specialists at the same pace, the buyer sees less operating leverage.

Another discount driver is weak evidence of recurring demand. Many founders describe customer relationships as recurring, but buyers will test it. They will ask for cohort data, renewal rates, customer tenure, contract terms, and revenue by customer over time.

Accreditation or quality issues can also create a heavy discount. In this sector, trust is the product. If there are unresolved audit findings, regulatory disputes, certification quality concerns, or customer claims, buyers will either reduce price, demand protections, or walk away.

7. Valuation Example: A Compliance and Certification Services Company

Let’s apply the logic to a fictional company.

Assume “HarborCert Assurance” is a fictional compliance and certification services provider with USD 10m of revenue. It serves regulated industrial and manufacturing customers, provides certification support, audits, technical compliance training, and recurring assurance services. The company and revenue level are fictional. The valuation ranges below are illustrative and are not investment advice or a formal valuation.

Step 1: Select the Right Comparables

The first mistake would be to value HarborCert like a pure regulatory software company if most of its revenue comes from services. The software and compliance management systems group in the data shows higher multiples, but that is not the right primary anchor unless HarborCert has real subscription revenue, scalable product margins, and software-led customer workflows.

A better starting point is the services-led compliance and certification universe. Public TIC and certification companies suggest a broad public reference area of roughly 1.1-3.3x revenue across relevant listed examples, with group averages around 2.0-3.2x depending on segment.

Private consulting, technical compliance, and training transactions suggest a broad range around 0.9-2.9x revenue, with higher outcomes for more recurring, higher-margin, and strategically attractive businesses.

Step 2: Narrow the Range

For a services-led certification and assurance company with some recurring revenue, a defensible core range might be around 1.8-2.8x revenue.

That range reflects both sides of the story. On the positive side, HarborCert has compliance demand, recurring certification work, and regulated customers. On the negative side, it is not clearly a software platform, and its growth still depends heavily on expert delivery.

If HarborCert has negative EBITDA, for example a USD 1.2m EBITDA loss on USD 10m revenue, the buyer would likely push toward the lower end unless there is a clear explanation. That would imply a negative 12% EBITDA margin, which creates real valuation pressure.

Step 3: Apply Scenarios

The software-led case should only be used if the facts support it. That means real subscription revenue, high gross margin, strong retention, scalable product delivery, and embedded customer workflows. A services business with a customer portal is not automatically a software business.

For founders, the key lesson is simple: two companies with USD 10m of revenue can be worth very different amounts. One may be worth under USD 15m if it is shrinking, unprofitable, founder-dependent, and project-based. Another may be worth over USD 35m if it is growing, recurring, high-margin, specialized, and strategically scarce.

Multiples are not magic numbers. They are shorthand for buyer confidence.

8. Where Your Business Might Fit Self-Assessment Framework

Use this as a practical self-assessment. Score each factor from 0 to 2.

0 means weak or not proven.1 means acceptable but not best-in-class.2 means strong and well-documented.

A rough interpretation:

Be honest. The goal is not to flatter yourself. The goal is to find the 3-5 improvements that could have the biggest impact before a sale.

If you score low on recurring revenue, focus on renewals, retainers, and subscription-style offerings. If you score low on financial clarity, clean up reporting. If you score low on management depth, reduce founder dependence. If you score low on margin, identify where delivery effort is not being priced properly.

9. Common Mistakes That Could Reduce Valuation

The biggest mistake is rushing the sale. A sale process exposes every weakness in the business. If your numbers, story, customer data, and management team are not prepared, buyers will either reduce price or lose interest.

Another mistake is hiding problems. Issues almost always surface in due diligence. Customer concentration, margin decline, accreditation concerns, employee turnover, legal disputes, or revenue recognition problems are better handled directly. Hiding them destroys trust and can reduce value late in the process.

Weak financial records are especially costly. In compliance and certification services, buyers want to understand revenue by service line, customer, geography, renewal status, gross margin, and delivery cost. If those numbers are unclear, the buyer will assume more risk.

Not running a structured, competitive process can also reduce valuation. Industry research and practical deal experience show that advisor-led competitive processes often lead to meaningfully higher purchase prices, commonly cited around 25%. The reason is simple: buyers behave differently when they know they are not the only option.

Revealing the price you want too early is another costly mistake. If you say you want USD 10m, buyers may offer USD 10.1m or USD 10.2m. You have killed price discovery. A well-run process lets the market reveal what strategic buyers are actually willing to pay.

Industry-specific mistakes include overstating “recurring revenue” without proof and calling the business “software-enabled” without real software economics. Buyers will test both. If the data does not support the claim, credibility suffers.

10. What Compliance and Certification Services Founders Can Do in 6-12 Months to Increase Valuation

You do not need to transform the whole company before selling. But you can improve the parts buyers care about most.

10.1 Improve the Numbers

Start with margin clarity. Break revenue and gross profit by service line: certification, audit, testing, training, consulting, software, retainers, and renewals. Buyers want to know which parts of the business are most attractive.

Review pricing. Many compliance services businesses undercharge for expert time, urgent delivery, specialized certifications, and complex regulated work. Even modest price increases can improve EBITDA if customer retention is strong.

Clean up one-time costs and owner-related expenses. Buyers will review adjustments carefully, so make sure they are real, documented, and easy to explain.

10.2 Make Revenue More Predictable

Convert repeat projects into formal renewal programs. Turn annual compliance work into multi-year contracts where possible. Create retained support packages for customers who need ongoing audit-readiness, regulatory monitoring, or training refreshes.

Track retention by customer cohort. Show how much revenue from last year returned this year. Buyers value proof more than narrative.

If you have training revenue, package it into recurring corporate programs rather than one-off course sales. If you have certification revenue, track renewal cycles and attach rates for related services.

10.3 Prove You Are Mission-Critical

Document why customers buy from you. Is it required by law? Required by their customers? Required for market access? Required to pass audits? Required to reduce safety or environmental risk?

Build case studies around regulated outcomes. For example: helped a manufacturer maintain certification, supported a life sciences audit, reduced compliance delays, or enabled entry into a new market.

The clearer the “must-have” story, the stronger the buyer narrative.

10.4 Reduce Founder Dependence

Before a sale, buyers want to see that the business can run without you.

Move key customer relationships to a broader team. Document technical delivery processes. Build a second layer of leadership across sales, operations, finance, and technical delivery.

If you are still approving every proposal, handling every major client issue, and leading every strategic relationship, buyers will see transition risk.

10.5 Build Scalable Delivery

Standardize repeatable work. Create templates, checklists, audit workflows, customer portals, training content, and internal knowledge bases.

This does not require a massive software build. Even simple workflow improvements can show buyers that the business can scale without adding senior headcount at the same pace as revenue.

If you already have software tools, measure their impact. Track usage, renewal, gross margin, delivery hours saved, and customer retention.

10.6 Prepare the Sale Story

Your sale story should not be “we are a good compliance business.” It should be more specific.

For example: “We are a recurring certification and technical compliance platform serving regulated manufacturing customers, with strong renewal behavior, specialized expertise, and clear expansion opportunities in training and audit-readiness.”

That kind of positioning helps buyers understand why the business matters and why it may be worth more than a generic services firm.

11. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor like Eilla AI can help founders run a broader, faster, and more disciplined sale process without losing the human judgment that matters in a high-stakes transaction.

The first advantage is buyer reach. AI can expand the buyer universe to hundreds of qualified acquirers based on deal history, strategic fit, financial capacity, sector focus, geography, and likely synergies. More relevant buyers means more competition, stronger offers, and a higher chance the deal closes even if one buyer drops out.

The second advantage is speed. AI-driven buyer matching, outreach support, marketing material preparation, and due diligence support can help founders reach initial conversations and offers in under 6 weeks. That does not mean cutting corners. It means removing manual bottlenecks from the process.

The third advantage is expert advisory enhanced by AI. You still need experienced human M&A advisors who know how to frame the business, manage buyers, negotiate terms, and protect value. AI supports that process by improving research, preparation, buyer targeting, and diligence readiness.

The outcome is Wall Street-grade advisory quality without traditional bulge bracket costs. If you would like to understand how our AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.