The Complete Valuation Playbook for Construction Equipment & Tool Rental Businesses

A practical breakdown of how construction equipment and tool rental businesses are valued and what drives premium multiples today.

Construction equipment and tool rental is no longer a simple “local yard with machines” business. Buyers now look at fleet age, utilization, specialty categories, branch density, digital booking, customer mix, service quality, safety record, and the ability to keep equipment earning revenue instead of sitting idle.

Now is an important time to think carefully about valuation. The sector continues to consolidate as large rental groups, equipment dealers, private equity firms, and specialty rental platforms look for attractive local and regional businesses. At the same time, buyers are more disciplined about debt, fleet capital needs, maintenance quality, and the true profitability of each branch.

This playbook shows what construction equipment and tool rental businesses actually sell for, what public markets imply, what pushes valuation higher or lower, and how you can assess your own company before going to market.

1. What Makes Construction Equipment & Tool Rental Unique

Construction equipment and tool rental businesses sit between services, logistics, asset ownership, and local market density. That makes valuation more complex than a simple revenue multiple.

The main types of companies in this sector include:

The big valuation difference is that equipment rental is asset-heavy. Buyers are not just buying your customer list and brand. They are also buying your fleet, your maintenance systems, your yard network, your delivery process, your people, and your ability to turn capital into rental revenue.

That means buyers will always check a few sector-specific risks. They will look at fleet age, repair history, utilization, customer concentration, safety incidents, delivery reliability, insurance claims, debt tied to equipment, and how much capital must be spent after closing to keep the fleet competitive.

A construction equipment rental business can look profitable on paper but still be less attractive if it has an aging fleet, poor maintenance records, underpriced long-term rentals, weak branch-level reporting, or too much revenue from one large contractor.

2. What Buyers Look For in a Construction Equipment & Tool Rental Business

Buyers start with the basics: revenue size, growth, EBITDA, margin stability, and cash flow. EBITDA means earnings before interest, taxes, depreciation, and amortization. In plain English, it is a common way buyers estimate operating profit before financing and accounting choices.

But in this sector, the deeper questions are more specific:

Do your customers rent repeatedly?Do they use you because you are the cheapest, or because you are reliable?Is your fleet young enough to keep working without heavy near-term spending?Can your team track utilization by asset, branch, and customer?Are your rates disciplined, or do you discount heavily to keep machines moving?

Strategic buyers often care about local density. If your branches fit into their existing map, they may see clear value: more fleet coverage, better delivery routes, cross-selling, and stronger local market share. A small rental company in the right geography can be worth more to the right buyer than a larger company in a less strategic market.

Private equity buyers think a little differently. They want to know whether they can buy your business at one valuation, improve it, and sell it later at a higher valuation. They ask: “Who could buy this in 3-7 years?” The answer might be a national rental group, a larger regional consolidator, another private equity firm, or a strategic equipment dealer.

How Private Equity Buyers Think

Private equity buyers usually focus on three questions.

First, can the business grow without breaking? A rental company that needs a huge amount of new equipment every year just to grow can be harder to scale than one with strong utilization, good pricing, and disciplined capital spending.

Second, are there clear improvement levers? These might include better pricing, route optimization, branch expansion, tuck-in acquisitions, cross-selling tools and consumables, improved repair processes, or better fleet purchasing.

Third, can the buyer sell the business later to a larger buyer? A company with clean numbers, a strong second layer of management, low customer concentration, and proven branch economics is easier to sell again.

3. Deep Dive: Fleet Quality, Utilization, and Specialty Mix

In construction equipment and tool rental, the biggest valuation nuance is this: buyers are not just paying for revenue. They are paying for productive assets that can keep generating revenue after the deal.

Two companies can both have USD 10m of revenue, but one may be worth far more if it has newer equipment, higher utilization, better maintenance records, and a more defensible specialty niche.

A broad general rental fleet can be attractive if it has strong local density and repeat contractor demand. But buyers often pay more attention when the company owns hard-to-source or mission-critical categories: lifting, access, power, climate control, pumps, trench safety, rail plant, temporary works, or highly specialized tools. These categories can support better pricing because customers care about availability, safety, and uptime more than the lowest day rate.

Utilization is also critical. A machine sitting idle is capital that is not earning. Buyers will want to see utilization by asset category, age, branch, and customer type. They will also want to understand whether strong utilization comes from healthy demand or from underpricing.

The best businesses can show that their fleet is both busy and profitable. That means good utilization, disciplined rental rates, controlled maintenance costs, and sensible capex planning. Capex means capital expenditure - money spent on equipment, vehicles, yards, and other long-term assets.

If your business looks more like the left column today, the goal is not to rebuild the company overnight. In 6-12 months, you can often improve valuation perception by cleaning fleet records, tracking utilization, tightening pricing, documenting maintenance, and showing which asset categories are most profitable.

4. What Construction Equipment & Tool Rental Businesses Sell For - and What Public Markets Show

The data shows a wide valuation spread. That is normal for this sector. Rental companies can look similar from the outside, but differ sharply in margins, fleet quality, specialty mix, growth, and capital intensity.

Public companies usually trade at higher multiples than small private companies because they have scale, access to capital, broader fleets, professional reporting, and better liquidity for investors. Private deal multiples are often lower, especially for smaller businesses, mixed rental-and-sales businesses, or companies with heavy customer concentration.

4.1 Private Market Deals - Similar Acquisitions

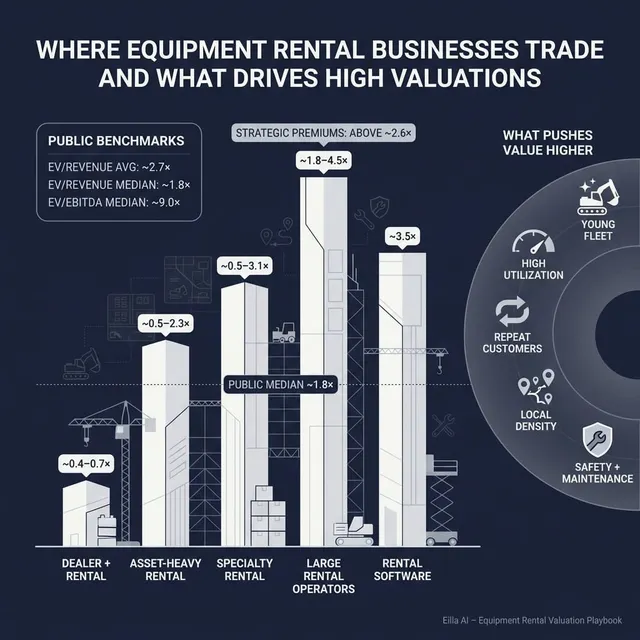

The private transaction data shows that asset-heavy rental, hire, and leasing providers often transact at lower revenue multiples than software or digital marketplace businesses. The overall private transaction average is about 1.8x revenue, while the median is about 0.7x revenue. On EBITDA, the average is about 5.4x and the median is about 3.6x.

That spread matters. It means founders should not anchor only on the highest deal headline. Many private rental businesses sell closer to the lower or middle part of the range unless they have strong margins, specialty exposure, scale, or a strategic location that a buyer badly wants.

The key lesson: revenue multiple alone can mislead you. A USD 20m revenue rental company with low margins, old fleet, and lots of equipment debt may be worth less than a USD 10m revenue specialty rental company with high EBITDA, strong utilization, and a young fleet.

For founders, private market data should be used as a practical starting point. If your business is a solid, local, asset-heavy rental company, the lower and middle parts of the private range may be most relevant. If you have strong specialty exposure, high margins, clean reporting, and a clear strategic buyer universe, you may deserve a premium.

4.2 Public Companies

Public market data gives a broader reference point. Across the public companies in and around equipment rental, leasing, specialty rental, dealers, modular rental, and asset finance, the overall average EV/Revenue is about 2.7x and the median is about 1.8x. The overall average EV/EBITDA is about 13.4x and the median is about 9.0x.

These figures are based on public company trading multiples around mid to end 2025. They should not be treated as a direct price tag for a private company. They are useful because they show how investors value different business models at scale.

The highest public multiples generally belong to companies with scale, strong market positions, predictable cash flows, and clear access to growth capital. Large rental groups also benefit from purchasing power, branch networks, national accounts, and sophisticated fleet management.

For a founder, public multiples are best used as an upper and lower reference band. A smaller private business usually receives a discount for size, liquidity, customer concentration, and reporting risk. However, a scarce, high-quality, specialty rental asset in a strategic geography can sometimes attract strong private buyer interest even if it is much smaller than the public companies.

5. What Drives High Valuations - Premium Valuation Drivers

Premium valuations usually come from reducing buyer risk while increasing buyer excitement. In equipment rental, the best deal stories combine strong numbers with a clear reason the buyer should care.

5.1 Specialty Categories With Real Pricing Power

Buyers tend to like rental businesses that are hard to copy. Lifting, access, climate control, power, pumps, rail equipment, temporary works, technical testing, and safety-related categories can be attractive because customers need reliability and compliance.

A contractor renting a basic tool may shop around for price. A contractor renting a crane, temporary power unit, or specialist access platform cares about availability, safety, operator knowledge, and avoiding jobsite delays. That can support better pricing and stronger customer loyalty.

5.2 Strong Fleet Utilization and Clean Asset Records

Buyers pay more when they can trust the fleet. That means clear records showing purchase dates, maintenance history, utilization, repair costs, downtime, and resale value.

A clean fleet story gives buyers confidence that they are not inheriting hidden capex. It also helps them underwrite the business more quickly. If a buyer can see which assets earn the best return, they can believe the growth story.

5.3 Recurring Customers and Repeat Rental Behavior

Rental revenue is not always contractually recurring, but it can be behaviorally recurring. A contractor who rents every month, across multiple job sites, and from several branches is valuable.

Buyers like to see repeat customers because it makes revenue easier to forecast. National accounts, regional contractors, municipalities, utilities, industrial customers, infrastructure customers, and maintenance clients can all improve the quality of the revenue base.

5.4 Branch Density and Local Market Position

Rental is a local business. Delivery time, pickup speed, emergency availability, and branch proximity matter.

A company with strong density in a city or region can be attractive to a larger consolidator. The buyer may be able to route deliveries better, share fleet across branches, expand into nearby markets, and cross-sell products.

5.5 Technology That Improves Operations

Technology does not automatically make a rental business worth a software multiple. But it can still improve valuation if it makes the rental operation more efficient.

Examples include online booking, real-time fleet availability, customer portals, GPS tracking, automated maintenance schedules, digital contracts, utilization dashboards, and integrated billing. Buyers care when technology improves margins, reduces downtime, increases customer retention, or makes the business easier to scale.

5.6 Clean Financials and Management Depth

Clean financials are a valuation driver because they reduce doubt. Buyers want to understand revenue by category, gross margin by branch, EBITDA adjustments, equipment debt, maintenance expense, capex, customer concentration, and working capital.

A strong leadership bench also matters. If the founder is the only person who can price jobs, manage key accounts, approve maintenance, negotiate purchases, and run branches, buyers will discount the business. If the team can operate without you, the company becomes less risky.

6. Discount Drivers - What Lowers Multiples

The biggest discount driver is uncertainty. If buyers cannot understand your numbers, your fleet, your margins, or your customer relationships, they protect themselves by lowering the price.

Common discount drivers in construction equipment and tool rental include:

A rental business can also be discounted if revenue growth has come from aggressive equipment purchases without proof that the fleet earns attractive returns. Buyers do not just want growth. They want profitable growth.

Another issue is underpriced long-term rentals. Long rental periods can look stable, but if rates are too low, the business may be locking assets into weak returns. Buyers will compare rental revenue against fleet value, maintenance cost, and replacement cost.

Businesses with lots of used equipment sales can also be harder to value. Used sales may be important and profitable, but buyers will separate repeat rental earnings from one-time equipment sale gains. If your EBITDA depends heavily on gains from selling equipment, buyers may discount it.

7. Valuation Example: A Construction Equipment & Tool Rental Company

Let’s use a fictional company called IronBridge Rental Co. This company and its USD 10m revenue level are fictional. The valuation range below is illustrative only. It is not investment advice, not a formal valuation, and not a fairness opinion.

IronBridge is a regional construction equipment and tool rental company with three branches. It rents compact equipment, aerial lifts, power tools, generators, and temporary site equipment to small and mid-sized contractors. It has basic online booking, decent utilization tracking, and a growing base of repeat customers.

Step 1: Choose the Right Benchmark Set

The first mistake would be to value IronBridge like a software company. Even if it has online booking and fleet software, it still owns and rents physical equipment. That means the most relevant benchmarks are equipment rental, tool rental, specialty rental, and asset-heavy hire businesses.

The private market data suggests many asset-heavy rental businesses transact around 0.5x-2.3x revenue, with overall private transaction averages around 1.8x revenue and median levels closer to 0.7x revenue. Public rental and related businesses trade higher, with overall public averages around 2.7x revenue and medians around 1.8x revenue.

For IronBridge, the core valuation range should not jump to software-like levels. But a premium to the lower private median may be reasonable if the business has good margins, strong utilization, repeat customers, clean financials, and a well-maintained fleet.

Step 2: Apply the Logic to USD 10m Revenue

Assume IronBridge has USD 10m of annual revenue.

The strong case could be defensible if IronBridge has strong EBITDA margins, younger fleet, good utilization data, specialty categories, repeat contractor customers, and a strategic branch footprint.

The discounted case may apply if IronBridge has old equipment, weak maintenance records, low margins, heavy debt, poor reporting, or too much revenue from one or two customers.

Step 3: Cross-Check With EBITDA

Revenue multiples are useful, but buyers will also look hard at EBITDA.

If IronBridge has USD 10m of revenue and a 25% EBITDA margin, that means USD 2.5m of EBITDA. Applying a 5.0x-7.0x EBITDA range would imply USD 12.5m-17.5m. A stronger business with specialty exposure and higher margins might support more. A weaker business might support less.

This is why two rental businesses with the same revenue can have very different values. A USD 10m company with low margins and old fleet may be worth less than USD 12m. A USD 10m company with strong margins, clean systems, young fleet, and strategic buyer interest may be worth USD 18m-26m or more.

The point is not that every USD 10m rental company is worth USD 18m-26m. The point is that valuation depends on the quality of the revenue, the quality of the fleet, and the buyer’s confidence in future earnings.

8. Where Your Business Might Fit - Self-Assessment Framework

Use this as a practical self-check before going to market. Score each factor from 0 to 2.

0 means weak or not proven.1 means acceptable but not best-in-class.2 means strong and well-documented.

How To Interpret Your Score

If you score 0-6, you may still be saleable, but buyers will likely focus on risk. You may want to spend 6-12 months improving reporting, fleet records, customer concentration, and margin visibility before launching a process.

If you score 7-10, you are likely in the fair market zone. The business may attract buyer interest, but valuation will depend heavily on growth, profitability, and competitive tension in the sale process.

If you score 11-12, you may have a premium-quality business. You probably have a stronger chance of attracting strategic buyers, private equity-backed platforms, or regional consolidators that see your company as more than just a fleet purchase.

Be honest. The value of this exercise is not to flatter yourself. It is to identify which improvements could have the biggest payoff before a sale.

9. Common Mistakes That Could Reduce Valuation

Rushing the Sale

A rushed sale usually leads to a weaker outcome. Buyers need clear numbers, a strong story, and time to compete. If you go to market before preparing your financials, fleet data, customer analysis, and growth story, you give buyers reasons to discount the business.

Hiding Problems

Problems almost always surface in due diligence. Due diligence is the buyer’s detailed review of your company before closing. If you hide customer losses, safety issues, equipment problems, tax concerns, or margin pressure, buyers lose trust.

The better approach is to identify issues early, explain them clearly, and show what you have done to fix them.

Weak Financial Records

Weak financial records are especially costly in this sector because buyers need to separate rental revenue, equipment sales, parts, service, delivery fees, repairs, maintenance, depreciation, equipment debt, and capex.

In 6-12 months, many founders can improve value perception by cleaning up revenue categories, tracking branch profitability, separating recurring rental income from one-time sales, and documenting add-backs. Add-backs are expenses that may not continue after a sale, such as certain one-time or owner-specific costs.

No Structured Competitive Process

Selling to the first buyer who calls is rarely the best way to discover value. A structured, competitive process with an advisor usually creates more buyer tension, better timing, cleaner materials, and stronger negotiating leverage. Research and market experience often point to meaningfully higher purchase prices - commonly cited around 25% - when a well-run advisor-led process creates real competition.

Revealing Your Target Price Too Early

If you tell buyers, “I want USD 10m,” you may anchor the process too low. Buyers may come back at USD 10.1m or USD 10.2m even if the market could have supported more.

A good sale process lets the market speak first. The goal is price discovery - finding out what qualified buyers are actually willing to pay when they know others are competing.

Ignoring Fleet Capex Reality

Some founders overstate cash flow by ignoring the real cost of replacing equipment. Buyers will not ignore it. If the fleet is old, under-maintained, or heavily financed, they will adjust the price.

Not Tracking Utilization by Asset Category

Revenue growth is not enough. Buyers want to know which assets actually make money. A high-revenue fleet category with low utilization and high repair costs may be less valuable than a smaller specialty category with strong returns.

10. What Construction Equipment & Tool Rental Founders Can Do in 6-12 Months to Increase Valuation

Improve the Numbers

Start by cleaning your financial reporting. Separate rental revenue, equipment sales, delivery, damage waivers, parts, repairs, service, and other income. Buyers should be able to understand what is repeatable and what is one-time.

Track EBITDA by branch if possible. If that is too difficult, at least track revenue, gross margin, maintenance expense, and fleet utilization by branch and category.

Review pricing. Many rental companies have legacy discounts that no longer make sense. Even small pricing improvements can have a meaningful effect on EBITDA if customer churn stays low.

Improve the Fleet Story

Create a fleet schedule that includes purchase date, original cost, book value, estimated market value, utilization, repair history, and maintenance status.

Identify old or underperforming assets. Selling weak assets, refreshing key categories, and documenting preventive maintenance can make the business look more controlled and less risky.

Show buyers that capex is planned, not chaotic. A simple 12-24 month fleet plan can help buyers understand what investment is needed after closing.

Improve Customer Quality

Reduce customer concentration where possible. If one contractor represents too much revenue, buyers will worry about losing that account.

Build evidence of repeat behavior. Show rental frequency, average customer life, top customer trends, and growth by customer cohort. A cohort is simply a group of customers that started renting from you in the same period.

Strengthen relationships with municipal, infrastructure, industrial, utility, and commercial contractors where relevant. These customers can make the revenue base feel more durable.

Improve the Management Bench

Document key processes: pricing, dispatch, maintenance, customer onboarding, collections, safety checks, and fleet purchasing.

Give more responsibility to branch managers and operations leaders. Buyers pay more when they believe the company can succeed after the founder steps back.

If you are still the only person managing every major customer, start transitioning relationships carefully before the sale process begins.

Improve the Buyer Story

Prepare a clear growth plan. Buyers want to understand where growth will come from: new branches, higher utilization, specialty categories, pricing, cross-selling, larger accounts, or acquisitions.

Make the story specific. “We can grow” is weak. “We can add trench safety and temporary power across our three branches because 40% of existing customers already rent adjacent equipment” is stronger.

11. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor like Eilla AI can help founders run a broader, faster, and more disciplined exit process without losing the human judgment that matters in a high-stakes sale.

AI can expand the buyer universe to hundreds of qualified acquirers based on deal history, strategic fit, financial capacity, geography, equipment category focus, and likely synergies. More relevant buyers means more competition, stronger offers, and a better chance the deal still closes if one buyer drops out.

AI-driven buyer matching, outreach support, marketing material creation, and due diligence preparation can also help accelerate the process. In many cases, initial conversations and offers can be reached in under 6 weeks because the manual work of buyer identification, positioning, and preparation is compressed.

The best outcome still requires expert human advisors. Experienced M&A professionals know how to frame the story, manage buyers, protect competitive tension, negotiate structure, and avoid common process mistakes. AI enhances that work by making it faster, broader, and more data-driven.

The result is Wall Street-grade advisory quality without traditional bulge bracket costs. If you would like to understand how an AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.