The Complete Valuation Playbook for Decarbonization Software Businesses

A practical guide to how decarbonization software businesses are valued and what drives premium multiples.

If you run a decarbonization software business and are thinking about a sale in the next 1-12 months, valuation is probably one of the hardest questions to answer honestly.

The market is active, but not simple. Buyers are interested in carbon accounting, energy management, ESG reporting, compliance, building optimization, and sustainability data platforms. At the same time, they are much more selective than they were during the peak software funding market. They are paying up for sticky, recurring, mission-critical software, but discounting businesses that still look like consulting, implementation, or carbon-project services.

This playbook is designed to help you understand what decarbonization software businesses actually sell for, what drives higher or lower multiples, and how to assess where your business might sit before going to market.

1. What Makes Decarbonization Software Unique

Decarbonization software sits at the intersection of software, regulation, energy, data, and corporate strategy. That makes valuation more nuanced than a standard vertical SaaS company.

The main types of companies in the sector usually include:

The best businesses in this sector are not just “dashboards.” Buyers want platforms that sit inside recurring workflows. For example, a tool that helps a customer report emissions once a year is less valuable than a system that becomes the ongoing source of truth for emissions, energy usage, supplier data, audit evidence, and compliance reporting.

Revenue models also vary. Some businesses are true subscription software, with annual contracts and high gross margins. Others have a mixed model: software license plus onboarding, data cleanup, consulting, carbon planning, or implementation support. A mixed model is not automatically bad, but buyers will separate software revenue from people-heavy services when deciding what multiple to pay.

The biggest risk factors buyers check are sector-specific. They will ask whether your carbon data is accurate, whether your reporting workflows match regulation, whether your software can handle new standards, whether customers renew after the first reporting cycle, and whether your value is tied to a temporary regulatory deadline or a long-term operating need.

2. What Buyers Look For in a Decarbonization Software Business

Buyers start with the obvious questions: How big is the business? How fast is it growing? Is revenue recurring? Are customers renewing? Is the company profitable or on a credible path to profitability?

But in decarbonization software, buyers go deeper. They want to know whether your product is a “must-have” or a “nice-to-have.” A must-have product helps customers meet compliance deadlines, lower energy costs, reduce operational risk, or manage data they cannot easily manage in spreadsheets. A nice-to-have product produces reports, dashboards, or sustainability insights that customers may cut when budgets tighten.

The strongest businesses usually show several traits:

Strategic buyers often care about product fit. They may already own reporting, energy management, enterprise resource planning, risk, compliance, or facilities management software. A decarbonization software company can be attractive if it fills a product gap and can be sold into their existing customer base.

Private equity buyers think slightly differently. They are asking: “If we buy this business today, who can we sell it to in 3-7 years, and at what valuation?” They care about the entry multiple, the future exit multiple, and the levers they can pull in between. Those levers may include better pricing, stronger sales processes, cross-selling new modules, buying smaller competitors, improving margins, or expanding into new geographies.

For private equity, the ideal business is not just “growing.” It is predictable. They want to see a path from today’s revenue to a much larger, cleaner, more profitable company that a strategic buyer or larger fund would want later.

3. Deep Dive: Software System of Record vs. Services Wrapper

One of the most important valuation questions in decarbonization software is this: are you really a software system of record, or are you a services business with software attached?

This distinction shows up clearly in the transaction data. Software and regulatory-content businesses in the dataset achieved meaningfully stronger outcomes than consulting-heavy environmental, energy, and carbon advisory businesses. The software businesses were valued for recurring workflows, high gross margins, and strategic platform fit. The consulting businesses were valued more like service providers, even when they operated in compliance-heavy markets.

Buyers care because software scales differently. Once the platform is built, adding another customer should not require a matching increase in consultants. A consulting-heavy model depends more on people, utilization, project delivery, and founder relationships. That lowers the multiple because growth is harder to scale and margins are usually less predictable.

The better version of the business is not “no services ever.” In this sector, some services are normal. Customers may need onboarding, data mapping, emission factor setup, supplier engagement, or implementation support. The question is whether those services are a temporary bridge to recurring software revenue, or whether they are the real engine of delivery.

If your business looks more like the left column today, the next 6-12 months should focus on proving software economics. Separate software and services revenue in your reporting. Productize implementation. Reduce manual work. Show that customers renew because the platform is embedded, not because your team keeps doing custom work behind the scenes.

4. Deep Dive: Regulation Is Valuable Only When It Creates Recurring Workflow

Regulation is one of the biggest demand drivers in decarbonization software. Rules around climate disclosure, carbon reporting, supplier due diligence, energy efficiency, and sustainability reporting are pushing companies to replace spreadsheets with software.

But buyers do not pay a premium just because your market is regulated. They pay a premium when regulation creates repeatable, sticky software usage.

There is a major difference between “we help customers comply” and “our platform is the system customers use every month to stay compliant.” The first can still look like advisory work. The second can look like a high-value software platform.

The strongest regulatory software businesses usually do three things well. First, they keep customers updated as rules change. Second, they connect reporting requirements to real business data. Third, they create evidence trails that make audits, board reviews, and external reporting easier.

For founders, this matters because regulation can be a strong valuation story, but only if you can prove it creates retention. Buyers will ask whether customers keep paying after the first reporting deadline. They will also ask whether your software becomes more valuable as rules become more complex.

A simple way to frame it:

The best positioning is not “we are exposed to climate regulation.” It is “regulation makes our product harder to replace every year.”

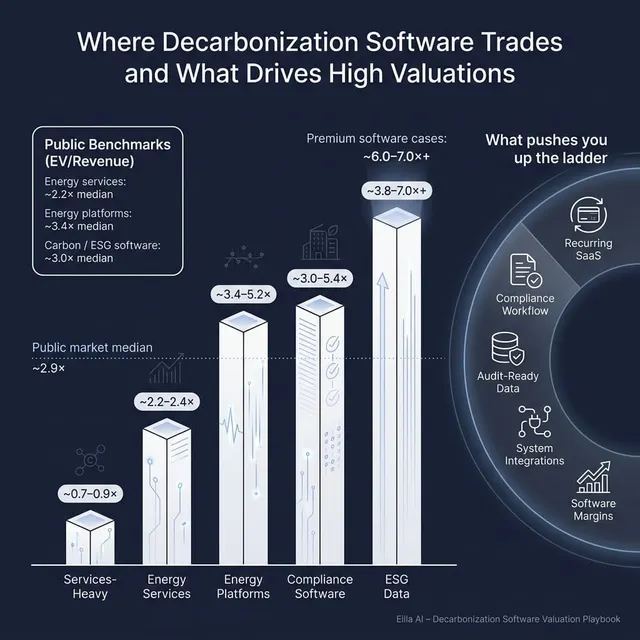

5. What Decarbonization Software Businesses Sell For - and What Public Markets Show

The valuation data shows a wide spread. That is normal in this sector because the market includes pure software, energy services, carbon-credit project developers, compliance tools, infrastructure technology, and consulting businesses.

For founders, the key point is simple: the headline market multiple is less important than the category buyers place you in. A pure recurring carbon accounting platform will not be valued the same way as a project-based energy consultancy or a carbon offset developer.

5.1 Private Market Deals - Similar Acquisitions

The private transaction data shows an overall average EV/Revenue multiple of around 3.0x and a median of around 2.5x. But that overall number hides a major split.

Environmental, energy, and carbon consulting or technical services transactions were much lower, with average and median EV/Revenue around 0.7x-0.9x and EV/EBITDA around 4.9x. By contrast, energy management, sustainability, and asset optimization software transactions were much higher, around 5.2x EV/Revenue on average and median. Regulatory compliance and sustainability monitoring software also showed around 5.4x EV/Revenue and about 20.8x EV/EBITDA.

This is why positioning matters. If buyers see you as a true decarbonization software company, the relevant private range may be closer to the software and compliance categories. If they see you as a consulting-led company with a software layer, they will likely anchor lower.

Deal size also matters. Smaller companies can achieve strong multiples when they own a focused niche, have recurring revenue, and fit a strategic buyer’s roadmap. But small companies with weak margins, customer concentration, or heavy delivery requirements are usually discounted.

These ranges are illustrative. They are not a formal valuation opinion. Your actual outcome will depend on growth, retention, margins, revenue quality, customer mix, buyer appetite, and how competitive the sale process is.

5.2 Public Companies

Public company multiples provide a useful reference point, but they are not a direct price tag for your private business. Public companies are usually larger, more liquid, better diversified, and easier for investors to buy and sell. That normally means private companies need a discount unless they are scarce, strategic, and growing quickly.

The public market data as of mid/end 2025 shows a very wide range. Overall average EV/Revenue was around 10.7x, but the median was much lower at around 2.9x. That gap tells you the average is being pulled up by outliers, including very small or highly valued data and decarbonization technology companies.

The software categories look more attractive than services-heavy categories, but founders should be careful with the averages. In carbon / ESG reporting and compliance software, the average EV/Revenue of 33.3x is much higher than the median of 3.0x. That suggests a few unusual companies distort the headline number.

Building and enterprise energy management platforms appear more stable, with average EV/Revenue around 3.9x and median around 3.4x. Energy efficiency and carbon compliance services sit lower, with median EV/Revenue around 2.2x. Carbon credits and environmental markets are highly variable, which makes sense because these businesses often carry project, commodity, regulatory, and execution risk.

For founders, public multiples should be used as a reference band, not a promise. A smaller private company will usually be adjusted down for lower scale, less liquidity, customer concentration, or weaker controls. But a scarce, fast-growing, highly strategic software asset can sometimes trade above the simple public median if multiple buyers see it as a must-have acquisition.

6. What Drives High Valuations - Premium Valuation Drivers

High valuations in decarbonization software are not random. They usually come from a few clear patterns that buyers recognize and believe they can scale.

6.1 Mission-Critical Compliance Workflows

Buyers pay more when your software helps customers meet mandatory reporting, compliance, audit, or disclosure obligations. This is especially powerful when the product is used repeatedly, not just once per year.

For example, a platform that tracks climate disclosure requirements across teams, stores evidence, updates rules, and produces audit-ready outputs is more valuable than a simple report generator. Buyers like products that become part of the customer’s compliance rhythm.

6.2 Pure Software Economics

Premium valuation requires software-like gross margins and limited human dependency. If every new customer requires a large amount of manual analyst time, buyers will question whether the business can scale.

Strong signs include automated data ingestion, repeatable onboarding, standard workflows, low support burden, and high gross margin. Services are acceptable when they support adoption, but they should not be the main value being sold.

6.3 Regulatory Complexity Turned Into Product

Regulation helps valuation when it becomes a product advantage. Cross-border rules, sector-specific reporting, ISO-related workflows, supplier requirements, and audit evidence can all create defensibility.

The key is productization. A consulting firm can understand regulation deeply, but a software company turns that knowledge into workflows customers can use repeatedly.

6.4 Strategic Fit With Larger Platforms

Some buyers pay more when the target fills a clear product gap. A decarbonization software company may be valuable to a buyer with financial reporting software, risk and compliance products, facilities management tools, energy procurement services, enterprise resource planning systems, or sustainability data platforms.

This type of premium is buyer-specific. It does not always show up in standalone financials. It shows up when an acquirer believes your product can be sold into their existing customer base or complete their broader platform.

6.5 Recurring Revenue Visibility

Buyers like revenue they can underwrite. That means annual recurring revenue, multi-year contracts, high renewal rates, and expanding customer spend over time.

A company with weak current EBITDA can still attract strong interest if buyers believe losses are a choice, not a structural problem. In plain English: buyers need to believe you could become profitable if you slowed hiring or sales investment.

6.6 Focused Niche Leadership

Small size is not always a disadvantage. A business that owns a specific niche - for example, carbon reporting for mid-market manufacturers, building energy optimization for commercial real estate, or supplier emissions tracking for regulated enterprises - can be valuable if the niche is growing and defensible.

Buyers like focus because it makes the story easier to understand. “We are the best product for this specific use case” often sells better than “we are a broad sustainability platform for everyone.”

6.7 Clean Financials and Strong Management

Even the best product can lose value if the numbers are messy. Buyers want clean revenue reporting, clear separation between software and services, reliable gross margin data, customer-level retention, and a leadership team that can operate without the founder doing everything.

A strong second layer of management reduces buyer risk. It tells buyers the business can survive the sale process and scale after closing.

7. Discount Drivers - What Lowers Multiples

The lower end of the valuation range usually comes from risk. Buyers do not just ask, “What could this business become?” They also ask, “What could go wrong after we buy it?”

The biggest discount driver in this sector is services dependency. If revenue depends heavily on custom consulting, manual data cleanup, one-off reporting projects, or senior experts, buyers will value the business more like a services company than a software platform.

Another common discount driver is weak retention. If customers buy because of a regulatory deadline and then churn after the report is complete, buyers will question whether the product is truly recurring. Strong renewal data is one of the best ways to fight this discount.

Other discount drivers include:

Carbon-credit exposure can also create valuation complexity. Buyers may discount businesses tied to offsets, project development, or environmental markets because revenue can depend on regulation, project delivery, credit pricing, and market trust.

Another issue is noisy market comparisons. Some public decarbonization and ESG data companies trade at very high revenue multiples because they are tiny, loss-making, or speculative. A buyer will usually not apply those outlier multiples to a private business unless the strategic rationale is unusually strong.

The good news is that many discount drivers can be improved. You may not be able to double revenue in 6 months, but you can improve reporting, separate revenue streams, reduce manual delivery, strengthen customer data, and tell a clearer story.

8. Valuation Example: A Decarbonization Software Company

Let’s apply the logic to a fictional company called CarbonLedger.

CarbonLedger is not a real company. The USD 10m revenue figure is also fictional. This example is only designed to show how valuation logic works. It is not investment advice, a fairness opinion, or a formal valuation.

Assume CarbonLedger sells carbon accounting and climate reporting software to mid-market and enterprise customers. It has mostly annual recurring revenue, some onboarding services, strong gross margin, and a growing compliance use case tied to climate disclosure and supplier emissions reporting.

Step 1: Choose the Right Comparable Set

The first step is deciding what category CarbonLedger belongs in. It should not be compared mainly with carbon-credit project developers, industrial decarbonization engineering companies, or environmental consulting firms. Those businesses have different risk profiles and economics.

The better anchors are:

Public software comps suggest a broad range. Carbon / ESG reporting and compliance software had a median EV/Revenue of around 3.0x, while selected software-like public names showed a bracket around roughly 2.9x-7.5x. Some outliers were far higher, but those should be treated carefully because they may reflect tiny revenue bases, speculative expectations, or very different business models.

Private software transactions in the source data point closer to around 5.2x-5.4x EV/Revenue for energy management, sustainability, asset optimization, and regulatory monitoring software.

Step 2: Apply the Logic to USD 10m Revenue

For CarbonLedger, a reasonable core valuation range might be around 4.5x-6.0x revenue, or USD 45m-60m of enterprise value on USD 10m of revenue.

That range gives some discount to the highest public software outliers, but recognizes the stronger private software deal data. It also assumes CarbonLedger is a real software company, not a consulting business with a product interface.

A discounted case could apply if CarbonLedger has high churn, weak gross margin, heavy services revenue, or unclear compliance defensibility.

A base case could apply if it has solid growth, recurring revenue, decent margins, and credible product positioning, but is still subscale or has some delivery complexity.

A premium case could apply if it has strong revenue growth, high renewal rates, mostly software revenue, strong gross margin, multi-year contracts, low customer concentration, and a product that a strategic buyer clearly needs.

Step 3: What This Means for Founders

Two companies with the same USD 10m of revenue can be worth very different amounts.

One USD 10m business may be worth closer to USD 25m-35m if buyers see it as people-heavy, low-margin, or risky. Another may be worth USD 60m-70m+ if buyers see a scarce, high-retention, mission-critical software asset in a fast-growing compliance market.

That is why valuation work before a sale matters. You are not just selling revenue. You are selling revenue quality, growth durability, margin potential, customer stickiness, strategic fit, and buyer confidence.

9. Where Your Business Might Fit - Self-Assessment Framework

Use this as a rough self-assessment, not a scientific scorecard. Score each factor from 0 to 2.

0 means weak or not proven. 1 means acceptable but not best-in-class. 2 means strong and clearly supported by data.

A total score near the top suggests you may be closer to premium software multiples. A mid-range score suggests a fair market outcome, where process quality and buyer fit will matter a lot. A low score suggests you may benefit from improving the business before launching a sale.

Be honest. The goal is not to feel good about the score. The goal is to identify which improvements could have the biggest impact on valuation.

10. Common Mistakes That Could Reduce Valuation

Rushing the Sale

The fastest way to leave money on the table is to rush into buyer conversations before your numbers, story, and process are ready.

Buyers will ask for revenue by product, software vs services mix, gross margin, customer retention, churn, customer concentration, pipeline, and profitability. If you cannot answer cleanly, they will assume risk and lower the price.

Hiding Problems

Founders sometimes try to hide churn, weak margins, customer issues, product gaps, or founder dependency. This usually backfires.

Problems almost always surface in diligence. When they do, the buyer does not just adjust valuation for the problem itself. They also adjust for lost trust.

Weak Financial Records

Messy financials create doubt. This is especially painful because many improvements are possible in 6-12 months.

You can improve revenue recognition, split software from services, track gross margin by product line, clean up customer-level reporting, and build a basic set of key metrics. These changes can materially improve buyer confidence.

No Structured Competitive Process

A single-buyer process usually favors the buyer. They know you have fewer options, so they can move slowly, ask for more information, and pressure price later.

Research across M&A processes shows that running a structured competitive process with an advisor typically leads to meaningfully higher purchase prices, often around 25% higher. The logic is simple: more qualified buyers create more competition.

Revealing Your Target Price Too Early

Do not tell buyers what price you want before the market speaks.

If you say you are looking for USD 10m, buyers may come back at USD 10.1m or USD 10.2m even if they could have paid much more. You have killed price discovery. A better process lets buyers show what the business is worth to them.

Overstating the “AI” or “Climate” Story

Buyers are tired of vague AI and climate claims. They will test whether AI actually reduces manual work, improves product quality, or increases margin. They will also test whether climate demand translates into paid, recurring contracts.

A grounded story beats a hype story.

Failing to Prove Data Quality

In decarbonization software, data quality is central. Buyers will ask where emissions data comes from, how calculations are performed, how evidence is stored, and how the platform handles changing standards.

Weak data controls can make a software company look risky, especially if the product supports compliance reporting.

11. What Decarbonization Software Founders Can Do in 6-12 Months to Increase Valuation

Improve the Numbers Buyers Care About

Start by cleaning up the metrics buyers will use to judge quality.

Separate software revenue from services revenue. Track recurring revenue, churn, renewal rates, expansion revenue, gross margin, and customer concentration. Show monthly or quarterly trends, not just annual totals.

If services are material, explain them clearly. Are they implementation services that help customers adopt the platform? Or are they custom consulting that customers depend on forever? The first is easier to defend.

Make the Business Look More Like Scalable Software

Reduce manual delivery wherever possible. Automate data imports, standardize onboarding, create repeatable workflows, and document customer success processes.

A buyer should be able to see that adding the next USD 1m of revenue will not require a large increase in headcount.

Strengthen Retention and Contract Quality

Push for annual or multi-year contracts where possible. Improve renewal tracking. Identify customers with expansion potential and build case studies showing how accounts grow over time.

If customers renew because your platform is embedded in compliance, audit, energy, or reporting workflows, make that evidence obvious.

Clarify the Strategic Buyer Story

Map your product against likely acquirer categories. These might include ESG reporting platforms, financial reporting software companies, energy management platforms, risk and compliance software vendors, facilities management platforms, enterprise software companies, and environmental services groups.

For each buyer category, explain the strategic fit in plain language. What product gap do you fill? What customers could they cross-sell into? Why would owning you be better than building internally?

Prepare for Diligence Before It Starts

Create a clean data room before launching a process. Include financials, customer contracts, product materials, pipeline, cohort data, employee information, compliance documentation, and key operational metrics.

This does not just make diligence smoother. It signals professionalism, reduces buyer uncertainty, and helps protect valuation after offers come in.

12. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor can help founders run a broader, faster, and more competitive process without losing the human judgment that matters in a sale.

The first advantage is broader buyer reach. AI can help identify hundreds of qualified acquirers based on deal history, strategic fit, financial capacity, product adjacencies, geography, and likely synergies. More relevant buyers means more competition, stronger offers, and a higher chance the deal closes if one buyer drops out.

The second advantage is speed. AI-driven buyer matching, outreach support, marketing materials, and diligence preparation can help reach initial conversations and offers in under 6 weeks. That matters because momentum is valuable in M&A. Slow, manual processes often lose buyer attention.

The third advantage is expert advisory enhanced by AI. Human M&A advisors still drive positioning, negotiation, credibility with acquirers, and judgment. AI makes the process more efficient, but the founder still benefits from experienced advisors who know how to frame the business, prepare the numbers, and create competitive tension.

Eilla AI combines expert M&A advisory with AI-native process execution: broader buyer coverage, faster preparation, stronger deal framing, and Wall Street-grade quality without traditional bulge bracket costs. To understand how our AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.