The Complete Valuation Playbook for Facilities & Buildings Management Businesses

A practical guide to how facilities and buildings management businesses are valued, and what drives premium multiples today.

Facilities and buildings management is no longer just about keeping assets running. Buyers increasingly see the sector as a mix of recurring services, technical operations, compliance, field execution, asset data, and workflow software. That creates a wide valuation spread: two companies can serve similar buildings, but sell for very different multiples depending on how predictable, scalable, and software-enabled the business is.

Now is an important time to understand valuation because the market is consolidating. Large facilities services groups, property software platforms, construction technology companies, and private equity buyers are all looking for ways to own more of the building lifecycle. At the same time, buyers are more disciplined than they were in the low-interest-rate years, so they pay premiums only when the business is genuinely differentiated.

This playbook shows what Facilities & Buildings Management businesses actually sell for, what public markets imply, what pushes a company toward premium multiples, what pulls it down, and how you can think about your own valuation before going to market.

1. What Makes Facilities & Buildings Management Unique

Facilities & Buildings Management sits at the intersection of physical assets, people, software, compliance, and customer trust. That makes valuation more nuanced than in many other sectors.

A typical business in this market may fall into one of several categories. Some companies are service-heavy facilities operators: maintenance, engineering, cleaning, security, mechanical and electrical services, and technical building support. Others are software-first businesses: facilities management platforms, field service tools, digital checklists, compliance documentation, work order management, asset registries, and building operations software. Some are hybrids, combining technology with managed services or technical labor.

That distinction matters a lot. The data shows a clear gap between software-like businesses and labor-intensive services businesses. Software businesses can scale without adding the same amount of headcount. Service-heavy operators often need more technicians, engineers, supervisors, vehicles, insurance, and working capital as revenue grows. Buyers understand this, and they price accordingly.

Facilities & Buildings Management companies also serve different customer types. A business selling to commercial landlords has a different risk profile from one selling to hospitals, industrial plants, government buildings, schools, retail chains, data centers, or residential property managers. The more mission-critical the facility, the more buyers care about service quality, uptime, safety, and compliance.

There are several valuation considerations that are specific to this sector:

Buyers will always check a few sector-specific risks. They will look at contract length, renewal rates, service-level obligations, margin by contract, exposure to labor cost inflation, health and safety history, insurance claims, subcontractor reliance, and whether revenue is truly recurring or simply repeating project work.

They will also test whether the business owns an operating system of record or just sells a nice-to-have tool. In this sector, a system of record might be the platform where teams log work orders, inspections, maintenance history, compliance evidence, asset status, photos, signatures, and handover documents. That is more valuable than a tool that is used only occasionally.

2. What Buyers Look For in a Facilities & Buildings Management Business

Buyers start with the basics: scale, growth, profitability, retention, and quality of earnings. In simple terms, they want to know whether your revenue is growing, whether customers stay, whether margins are real, and whether the business can keep performing after you sell it.

For service-heavy companies, buyers focus heavily on contract quality. They want to know which contracts are multi-year, which are annually renewed, which are project-based, and which are vulnerable to rebid. A USD 10m revenue business with mostly contracted, recurring maintenance revenue will usually be seen as higher quality than a USD 10m business driven by one-off fit-out or construction projects.

For software-first companies, buyers look at customer stickiness, product usage, gross margin, growth rate, and how deeply the software sits inside daily workflows. A platform used every day by field technicians, property managers, contractors, and asset owners is more valuable than a dashboard that only a few managers open once a month.

Industry-specific buyer questions often include:

- Does the company manage live operational workflows or only reporting?

- Does the platform capture field data in real time?

- Are customers using the product for compliance, audits, inspections, defects, or mandatory documentation?

- Is revenue tied to buildings, users, assets, work orders, or transactions?

- Can the product or service expand from one site to many sites within the same customer?

- Are margins improving as the company scales?

Strategic buyers usually care about fit. They ask whether your business helps them sell more to their existing customers, enter a new geography, add a new workflow module, or deepen their position in the building lifecycle. A buyer with an existing property, construction, or facilities software platform may pay more for a product that immediately expands its suite.

Private equity buyers think slightly differently. They are buying today with a view to selling again in 3-7 years. They care about the entry multiple they pay now, the exit multiple they might receive later, and the improvements they can make in between. They may ask: Can we grow this business faster? Can we improve margins? Can we buy smaller competitors? Can we professionalize sales? Can this become attractive to a larger strategic buyer later?

For private equity, the most attractive Facilities & Buildings Management businesses usually have several levers: recurring revenue, fragmented competition, cross-sell potential, pricing power, a credible management team, and clear room for operational improvement.

3. Deep Dive: Software-Enabled Workflow vs Labor-Heavy Service Delivery

The most important valuation nuance in this sector is the difference between being a software-enabled workflow business and being a labor-heavy services business.

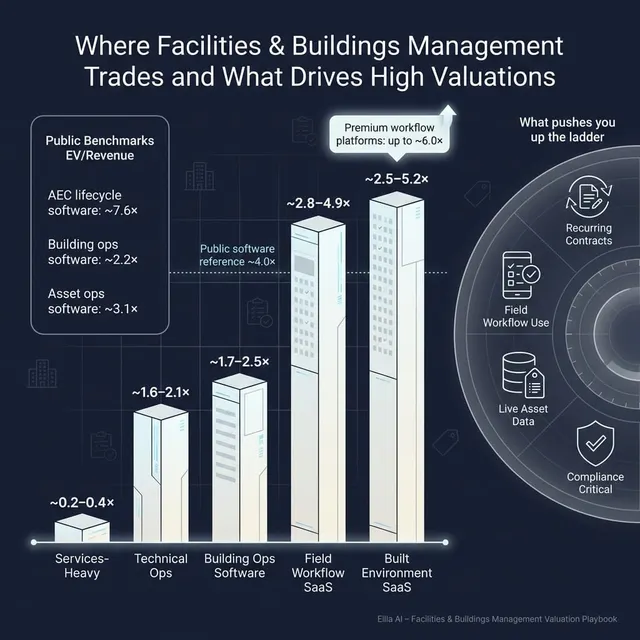

This difference shows up clearly in the transaction data. Built environment SaaS deals in the data averaged around 2.7x revenue and 15.5x EBITDA. By contrast, technical operations and services-heavy deals averaged around 2.1x revenue and 8.0x EBITDA. In plain English: buyers generally paid more for businesses where the product is scalable software and less for businesses where growth depends heavily on people and project execution.

That does not mean services businesses are bad. Many facilities services companies are excellent businesses. They can have loyal customers, strong cash flow, and defensive demand. But the valuation logic is different. If every extra dollar of revenue requires more staff, vehicles, supervisors, subcontractors, and working capital, buyers will usually apply a lower multiple than they would to software revenue.

The best-positioned companies often sit in the middle: they understand the real physical workflow of buildings, but use technology to make that workflow more scalable. Examples include mobile-first maintenance tools, digital inspection forms, asset registries, work order systems, real-time field reporting, incident capture, photo documentation, digital signatures, and compliance records.

Buyers pay attention to whether your technology is actually used at the point of work. A field technician logging maintenance actions on a mobile app, a facilities manager tracking asset history, or a contractor uploading compliance evidence from site all create operational data. That data makes the platform more embedded and harder to replace.

If your business looks more like the left column today, you do not need to become a pure software company overnight. But you can move toward the right column by productizing workflows, improving contract structure, tracking asset-level data, standardizing delivery, reducing manual reporting, and proving that customers rely on you for daily operations rather than occasional support.

4. What Facilities & Buildings Management Businesses Sell For - and What Public Markets Show

Valuation in this sector depends heavily on business model. A facilities software platform, a construction documentation tool, a technical engineering services company, and a property operations software provider may all touch buildings, but buyers do not value them the same way.

The data points to a broad range. Private transactions in the relevant built environment set averaged around 2.5x revenue and 10.5x EBITDA overall. But within that, software-like businesses commanded higher EBITDA multiples than services-heavy businesses. Public company multiples, as of mid to end 2025, show a similar pattern: AEC and construction lifecycle software trades at materially higher revenue multiples than property and facilities operations software or horizontal workflow software.

4.1 Private Market Deals - Similar Acquisitions

Private market data shows that built environment SaaS businesses, especially those tied to construction project management, documentation, quality, field execution, and compliance workflows, generally transact at stronger multiples than labor-intensive technical services businesses.

In the precedent transaction set, Built Environment SaaS deals averaged around 2.7x revenue and 15.5x EBITDA. Built Environment and Technical Operations Software/Services deals averaged around 2.1x revenue and 8.0x EBITDA, with the median revenue multiple closer to 1.6x. That gap is important for founders: being in the same end market is not enough. The delivery model drives valuation.

These ranges are illustrative, not a price tag. A founder should not look at one headline multiple and assume it applies directly. Buyers will adjust based on revenue quality, margins, growth, customer concentration, contract length, technology depth, and whether the business is scalable without adding the same level of headcount.

A practical takeaway: if you are a service-heavy facilities operator, EBITDA multiple may matter more than revenue multiple. If you are a software-first workflow platform with high gross margins and strong retention, revenue multiple may be more relevant.

4.2 Public Companies

Public market data gives another reference point. It does not directly determine what your private company is worth, but it helps buyers frame the market. Public companies are usually larger, more liquid, better known, and more diversified, so smaller private businesses often trade at a discount unless they are growing very quickly or are strategically scarce.

As of mid to end 2025, the public comp set shows clear differences by category. AEC and construction lifecycle software companies traded at the highest average revenue multiples. Property, facilities, and building operations software traded lower. Industrial and asset-intensive operations software sat in the middle. Horizontal workflow and document management software had lower revenue multiples than vertical AEC software, but some companies still showed strong EBITDA multiples where profitable.

The very high average EBITDA multiple for AEC software is influenced by the specific composition of the public group and should not be treated as a normal private company benchmark. Median figures are often more practical for founders because they reduce the impact of outliers.

For Facilities & Buildings Management founders, public multiples are best used as an upper and lower reference band. A smaller private company with slower growth, lower margins, or customer concentration will usually be valued below large public software companies. But a scarce asset with international reach, strong retention, real workflow depth, and strategic fit can still command a premium.

The key is not to ask, “What does the public market trade at?” The better question is, “Which public and private categories does my business most closely resemble, and what adjustments would a buyer make?”

5. What Drives High Valuations - Premium Valuation Drivers

Premium valuations are rarely caused by one thing. They usually come from a combination of growth, predictability, margin quality, strategic importance, and buyer competition. In Facilities & Buildings Management, the following themes matter most.

5.1 Workflow software embedded in a broader operating stack

Buyers pay more when your product is not a standalone point solution, but part of a broader operating workflow. In the data, the strongest software-like outcomes clustered around targets that could plug into larger construction, facilities, property, or small-business software platforms.

This matters because acquirers are often trying to expand wallet share. If they already sell accounting, scheduling, estimating, work order, or asset management tools, adding your workflow module may let them sell a more complete platform.

Practical examples include software that connects maintenance requests, field updates, inventory, billing, documentation, asset history, and customer communication. A simple task tool may be useful. A workflow layer that helps run the building is more strategic.

5.2 Asset-light SaaS economics

The data separates software economics from labor-heavy services. Businesses with productized software delivery achieved meaningfully stronger multiples than companies where revenue depended heavily on project labor, construction execution, or engineering headcount.

Buyers like software because gross margins can be high, revenue can repeat, and growth does not always require a matching increase in staff. For a founder, the question is simple: can you add revenue without adding the same amount of cost?

This does not mean you must eliminate services. Implementation, training, and support can be valuable. But if services dominate the business and software is only a small wrapper, buyers will usually value you more like a services company.

5.3 Mobile-first field execution and live site data

Facilities and building operations happen in the field. Buyers pay attention to products that capture work as it happens: photos, signatures, maintenance records, inspections, defects, incidents, asset status, and technician notes.

Mobile-first field execution creates stickiness because users build the operating history of a building inside the platform. Once a customer has years of asset records, inspection evidence, and maintenance history in one place, switching becomes painful.

This is especially important where the customer needs audit trails, health and safety records, regulatory evidence, or handover documentation.

5.4 Compliance and documentation workflows

Compliance-adjacent workflows often receive stronger buyer interest because they are closer to “must-have” than “nice-to-have.” In construction and facilities, documentation can include quality checks, safety inspections, incident reports, preventive maintenance evidence, certifications, audit trails, and digital signatures.

Founders should be able to show that customers rely on the product or service to avoid risk, not just to save time. A platform that helps customers prove work was done, prove inspections happened, and prove standards were followed can be much more valuable than a generic collaboration tool.

5.5 Cross-lifecycle product breadth

Buyers like businesses that cover more of the asset lifecycle: planning, construction, handover, operations, maintenance, compliance, and reporting. The broader the lifecycle coverage, the more ways a buyer can grow the account.

But breadth alone does not guarantee a premium. The data suggests that breadth is valuable only when paired with workflow criticality and software economics. A company can cover many stages of the building lifecycle but still receive a lower valuation if the model is services-heavy or not mission-critical.

The best version is a platform that starts with one urgent problem, wins trust, and then expands into adjacent workflows over time.

5.6 Geographic reach and repeatability

International or multi-region reach can support a premium when it proves that the product or model travels well. Buyers like repeatability. If your business works across customer types, building types, or geographies without heavy customization, it feels more scalable.

However, geographic reach is not automatically valuable. A services company spread across many regions can become harder to manage. A software platform with proven cross-border adoption is a stronger valuation story.

5.7 Clean financials and a strong leadership bench

Even if the product is attractive, buyers will discount messy numbers. Clean financials, clear revenue categories, reliable margin reporting, and well-documented contracts reduce buyer fear.

A strong leadership bench also matters. If the business depends too heavily on the founder for sales, customer relationships, product direction, or operations, buyers worry about what happens after closing. The less the business depends on you personally, the more valuable it usually becomes.

6. Discount Drivers - What Lowers Multiples

Discount drivers are not always fatal. Many can be fixed or reduced before a sale process. But buyers will price them in if they remain unresolved.

The first major discount driver is a services-heavy model. If revenue growth depends on adding people, subcontractors, vehicles, equipment, or project managers, buyers will usually apply lower multiples. The business may still be valuable, but it will be valued more on cash flow and margin stability than on software-style revenue.

The second is weak recurring revenue. Facilities Management businesses sometimes describe revenue as recurring because the same customers come back each year. Buyers will test that. They will ask whether contracts are signed, whether there are renewal terms, whether work is guaranteed, and whether revenue can disappear if a customer delays a project.

Customer concentration is another major issue. If one or two customers represent a large share of revenue or profit, buyers worry that losing one account could damage the business. This is especially sensitive in facilities services, where a large contract can look attractive but may carry thin margins, heavy staffing needs, and rebid risk.

Low gross margins or unclear margin reporting also hurt valuation. Buyers want to understand profit by customer, site, contract, service line, and product line. If the numbers are blended, they may assume the worst.

Other common discount drivers include:

In software businesses, buyers will also discount high churn, low product usage, heavy implementation burden, weak customer support, or a product that is easily replaced. In facilities services, they will discount poor safety records, labor disputes, underpriced contracts, insurance issues, and aggressive revenue recognition.

The practical point is this: buyers do not just buy your current revenue. They buy the confidence that revenue will continue, grow, and convert into cash after they own the business.

7. Valuation Example: A Facilities & Buildings Management Company

This example is fictional. The company, its revenue level, and the valuation ranges below are illustrative only. This is not investment advice, a formal valuation, or a fairness opinion.

Imagine a fictional company called NorthBridge Facilities Cloud. It sells software to facilities managers, commercial property operators, and technical maintenance teams. The platform manages work orders, inspections, asset records, digital checklists, field photos, compliance evidence, and reporting. It also has a small services team for onboarding and customer support.

Assume NorthBridge has USD 10m of annual revenue. It is software-first, has a meaningful recurring revenue base, serves customers across several countries, and is used by field teams as well as office-based facilities managers. It is not a contractor, engineering firm, or labor-heavy facilities operator.

Step 1: Select the right valuation reference points

For this type of company, the most relevant references are:

- Built environment SaaS private deals

- Property / facilities / building operations public software

- AEC / construction lifecycle software public companies

- Industrial / asset-intensive operations software companies

- Field service and maintenance workflow transactions

The least relevant references are pure construction contractors, engineering services companies, and labor-intensive facilities operators. They operate in related end markets, but their economics are different.

Step 2: Narrow the core multiple range

Based on the provided data, a defensible core revenue multiple range for a software-first built environment workflow business at USD 10m revenue might be around 2.5x-4.5x revenue.

The lower end is supported by private built environment SaaS transaction levels and sits above weaker property / facilities and generic workflow software references. The upper end is supported by the lower end of relevant public AEC software references, but discounted for smaller scale, private-company risk, and the lack of full public-company liquidity.

Step 3: Adjust for premium and discount factors

If NorthBridge has strong growth, high retention, clean recurring revenue, mobile-first field usage, compliance-critical workflows, and international repeatability, it could push toward the high end or above the core range.

If it has weak growth, low margins, high churn, heavy services revenue, poor financial reporting, or too much customer concentration, it may fall below the core range.

The lesson is simple: two companies with the same USD 10m of revenue can be worth very different amounts. One may be a low-margin, services-heavy operator with short-term contracts. Another may be a sticky, software-first platform used daily across customer operations. Buyers will not value those two businesses the same way.

For founders, this is why valuation preparation matters. You are not just trying to grow revenue. You are trying to improve the quality, predictability, margin profile, and strategic importance of that revenue.

8. Where Your Business Might Fit - Self-Assessment Framework

Use this as a rough self-assessment before going to market. Score each factor from 0 to 2:

- 0 = weak or not proven

- 1 = acceptable but improvable

- 2 = strong and well documented

This is not a formal valuation tool. It is a way to identify which areas are likely to move buyer perception.

A total score of 13-16 suggests you may be closer to a premium valuation profile, assuming the numbers support the story. A score of 8-12 suggests a fair market profile: saleable, but with clear areas to improve. A score below 8 suggests you may want to spend 6-12 months fixing valuation gaps before launching a process.

Be honest. The goal is not to give yourself a flattering score. The goal is to find the few improvements that could have the biggest effect on buyer confidence.

9. Common Mistakes That Could Reduce Valuation

The first mistake is rushing the sale. Buyers can tell when a company is not prepared. If your numbers are messy, your story is unclear, your contracts are disorganized, or your management team is not ready for diligence, you lose leverage.

The second mistake is hiding problems. Every business has issues. Maybe one customer is too large. Maybe churn increased. Maybe one contract has poor margins. Maybe a product module is underused. If you hide these problems, they will usually surface later in diligence. When that happens, buyers lose trust and often reduce price.

Weak financial records are another major mistake. Facilities and building operations businesses often have complex revenue streams: recurring software, implementation fees, service contracts, project work, subcontractor costs, pass-through costs, and hardware or equipment. If you cannot clearly show margin by revenue type, buyers may apply a discount.

Founders also underestimate the value of a structured, competitive sale process. Research and market experience consistently show that running a structured process with an advisor can lead to meaningfully higher purchase prices, often cited at around 25%, because competition improves price discovery and negotiating leverage. A single-buyer conversation may feel easier, but it often leaves money on the table.

Another mistake is revealing the price you want too early. If you tell buyers you are looking for USD 10m in enterprise value, many will anchor around that number and offer USD 10.1m or USD 10.2m. You may never discover that the right strategic buyer would have paid materially more. Let the market come back with offers.

There are also sector-specific mistakes. One is failing to separate recurring maintenance or software revenue from one-off project revenue. Another is not tracking safety, compliance, service-level performance, or contract-level profitability. In this sector, buyers care deeply about operational risk. If you cannot measure it, they will price it conservatively.

10. What Facilities & Buildings Management Founders Can Do in 6-12 Months to Increase Valuation

You do not need to transform the entire business before a sale. But you can make meaningful improvements in 6-12 months if you focus on the right areas.

Improve the numbers

Start by cleaning up revenue categories. Separate recurring software, recurring services, project revenue, implementation fees, subcontractor pass-throughs, and one-time work. Buyers should be able to see what revenue repeats and what revenue does not.

Track gross margin by service line, product line, customer, and contract. If some contracts are underpriced, identify them early. A buyer will find them anyway, so it is better to show a plan: repricing, renegotiation, scope adjustment, or exit.

Build a simple monthly KPI pack. Include revenue, gross margin, EBITDA, bookings, backlog, renewal rate, churn, customer concentration, sales pipeline, and contract wins. For software businesses, add usage, retention, expansion, and support metrics.

Improve revenue quality

Where possible, shift customers toward multi-year contracts, automatic renewals, or clearer recurring service agreements. Even small improvements in contract structure can help buyer confidence.

If you have project revenue, try to attach recurring maintenance, support, inspection, software, or reporting revenue. Buyers like when one-off work creates a long-term customer relationship.

Reduce customer concentration where you can. Winning new customers may not fully solve the issue in 6 months, but showing a stronger pipeline and reducing dependence on one account can help.

Strengthen the strategic story

Clarify what makes you more than a generic facilities provider or workflow tool. Are you the operating layer for compliance? The system of record for asset maintenance? The mobile field tool for inspections? The platform that connects buildings, technicians, owners, and contractors?

Document customer use cases. Buyers respond well to concrete examples: “This customer manages 300 sites on our platform,” or “This customer uses us for all preventive maintenance evidence,” or “This customer expanded from one region to five.”

If you have integrations, partnerships, or embedded workflows, make them visible. Integrations with property systems, accounting systems, asset management tools, construction software, or customer portals can strengthen the strategic case.

Reduce buyer risk

Build a stronger second layer of management. Buyers pay more when the business can run without the founder making every key decision.

Organize contracts, insurance documents, compliance records, employee agreements, customer lists, supplier contracts, and financial statements. A clean data room creates confidence and reduces deal friction.

Address obvious diligence issues before buyers find them. That may include revenue recognition, contractor classification, safety documentation, overdue receivables, margin leakage, or undocumented customer terms.

Prepare the sale narrative

The best sale processes do not just present numbers. They explain why the business matters, why now is the right time, who the natural buyers are, and how the company can grow under new ownership.

For Facilities & Buildings Management companies, the narrative should connect directly to buyer priorities: recurring revenue, building lifecycle coverage, field execution, compliance, asset data, customer stickiness, and scalability.

11. How an AI-Native M&A Advisor Helps

A strong M&A process is about more than finding a buyer. It is about finding the right buyers, creating competition, telling the story well, and managing the process so buyers stay engaged through diligence and offers.

An AI-native advisor like Eilla AI can expand the buyer universe to hundreds of qualified acquirers based on deal history, strategic fit, synergies, financial capacity, sector focus, and other signals. More relevant buyers usually means more competition, stronger offers, and a higher chance the deal closes because you have alternatives if one buyer drops out.

AI can also accelerate the early stages of a process. Buyer matching, outreach support, preparation of marketing materials, financial analysis, and diligence support can move faster than in a manual-only process. That can help founders reach initial conversations and offers in under 6 weeks, depending on readiness and market response.

The best model is not AI instead of advisors. It is expert human advisors enhanced by AI. Experienced M&A professionals still drive positioning, negotiation, buyer credibility, process strategy, and deal judgment. AI helps them work faster, search broader, and prepare better.

The outcome is Wall Street-grade advisory quality without traditional bulge bracket costs. If you would like to understand how an AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.