The Complete Valuation Playbook for Health, Wellness & Fitness Services Businesses

A data-driven guide to how health, wellness and fitness services businesses are valued and what drives premium multiples

If you run a health, wellness, fitness, physiotherapy, rehabilitation, or therapeutic services business, valuation is not just about your revenue. Buyers want to know what kind of revenue you have, how hard it is to replace, how much profit it produces, and whether the business can grow without depending entirely on you.

This matters now because the sector is consolidating. Larger fitness platforms, healthcare groups, occupational health providers, rehabilitation networks, wellness brands, and private equity buyers are all looking for assets that help them expand reach, add specialist services, or build more integrated care models.

This guide shows what health, wellness, and fitness services businesses actually sell for, what drives higher versus lower multiples, how public markets frame valuation, and what you can do in the next 6-12 months to improve your exit outcome.

1. What Makes Health, Wellness & Fitness Services Businesses Unique

Health, wellness, and fitness services sit in an unusual place. They are part consumer service, part healthcare, part local infrastructure, and sometimes part technology-enabled care. That makes valuation more nuanced than a simple “gym revenue multiple” or “clinic EBITDA multiple.”

The main types of companies in this sector include fitness clubs, boutique studios, franchise fitness platforms, physical therapy clinics, rehabilitation providers, chronic pain and musculoskeletal care businesses, occupational health providers, wellness centers, digital health platforms, and health equipment or mobility product companies.

Buyers usually separate these into two broad buckets. The first is site-based service businesses, where growth depends on locations, staff, utilization, and local demand. The second is more scalable or specialized businesses, where technology, clinical specialization, product IP, employer contracts, payer relationships, or franchise systems can support higher valuation.

A local gym with some physiotherapy services is not valued the same way as a multi-site rehabilitation network, a digital musculoskeletal care platform, or a specialized neuro-orthotics product business. The same USD 10m of revenue can be worth very different amounts depending on the mix.

Key valuation considerations include:

The biggest risk factors buyers check are customer churn, staff retention, regulatory compliance, reimbursement exposure, clinical quality, location economics, lease obligations, utilization rates, and whether revenue is truly repeatable.

For fitness clubs, buyers will focus on member growth, churn, membership pricing, location density, utilization, and cost of acquiring new members. For physiotherapy and rehabilitation businesses, they will look closely at clinician productivity, payer mix, referral sources, treatment outcomes, and compliance. For wellness and therapeutic services, they will ask whether the brand is differentiated or just another local consumer service business.

2. What Buyers Look For in a Health, Wellness & Fitness Services Business

Buyers start with the basics: revenue scale, growth, profitability, customer retention, clean financials, and management depth. A business that is growing steadily, producing healthy profit, and not overly dependent on one founder or one location will almost always be easier to sell.

But in this sector, the details matter. Buyers want to understand whether your revenue is supported by memberships, packages, employer contracts, physician referrals, insurance reimbursement, subscription programs, or walk-in demand. Recurring memberships and contracted services are usually more attractive than unpredictable one-off visits.

They also look at whether the business has a clear reason to exist. A general wellness brand with friendly messaging is not enough by itself. The data shows that approachable or holistic positioning can support customer appeal, but it does not automatically create premium valuation. Buyers pay more when the business has something harder to copy: specialized clinical pathways, strong local density, digital delivery, proprietary programs, deep referral channels, or a platform that fits neatly into a buyer’s strategy.

For gyms and studios, buyers care about unit-level performance. That means revenue per location, member count, churn, rent as a percentage of revenue, staff costs, class utilization, and whether new sites can be opened profitably. For therapy and rehab clinics, they care about appointment volume, clinician productivity, referral conversion, treatment mix, reimbursement quality, and patient outcomes.

How Private Equity Buyers Think

Private equity buyers are financial buyers. They buy businesses with the aim of improving them and selling them again later, often after 3-7 years. They care about what they pay today, what they can change during ownership, and who might buy the business from them later.

They think about the entry multiple and the exit multiple. In simple terms, if they buy your business at 6.0x EBITDA, they want to believe they can sell it later at the same multiple or higher. That might be possible if they can increase scale, improve margins, add sites, strengthen systems, and make the business more attractive to larger strategic buyers or bigger private equity funds.

Common value levers include price increases, better membership packaging, improved scheduling, centralized back-office functions, stronger marketing, cross-selling fitness and therapy services, acquiring smaller local competitors, and reducing founder dependency.

Private equity also cares about downside protection. If your business depends heavily on one location, one clinician, one referral source, or one charismatic founder, a buyer will see risk. If it has repeatable systems, a second layer of leadership, and strong monthly reporting, the buyer has more confidence.

3. Deep Dive: General Wellness Versus Specialized Care - Why the Difference Matters

One of the most important valuation lessons from the data is this: broad wellness positioning is not the same as strategic differentiation.

A business can be friendly, inclusive, holistic, and prevention-oriented, but that does not automatically make it a premium asset. Buyers have seen many wellness brands with attractive language but limited defensibility. If the service can be copied by another local operator, the valuation usually stays closer to service-business multiples.

Specialized care is different. Physical rehabilitation, chronic pain management, occupational health, neuro-orthotics, musculoskeletal care, employer health programs, and integrated therapy pathways can be more valuable because they solve more specific problems. They may also connect to healthcare systems, insurers, employers, or larger strategic acquirers in a clearer way.

This distinction shows up clearly in the source data. General fitness, gym-based wellness, and broad therapeutic services tend to trade at more modest revenue multiples unless they have scale, strong margins, or a strategic digital layer. More specialized care and rehabilitation-related assets can command higher interest when they add scarce capability or create a new category for the buyer.

Founders should not read this as “fitness is bad” or “wellness is low value.” That is not the point. The point is that buyers pay more when the business is hard to replace.

If your business looks more like the left column today, you can still move toward the right. Start by defining your strongest use cases. Are you best at post-surgery rehab, chronic back pain, women’s fitness, employer wellness, senior mobility, athletic recovery, weight management, or integrated gym plus physiotherapy care?

Then prove it with numbers. Track retention, outcomes, referral sources, package renewal rates, member engagement, treatment completion, and repeat visits. Buyers do not just want a good story. They want evidence.

4. What Health, Wellness & Fitness Services Businesses Sell For - and What Public Markets Show

Valuation data in this sector is wide because the sector itself is wide. A local gym, a national fitness chain, a physiotherapy clinic network, a hospital operator, a digital MSK platform, and a rehab product company are all technically related, but buyers do not value them the same way.

The right way to use the data is not to pick the highest multiple and apply it to your business. The right way is to ask: which companies in the data actually look like my business model, scale, growth profile, margin structure, and risk level?

4.1 Private Market Deals - Similar Acquisitions

The private transaction data shows a broad range, but the most relevant service-heavy deals cluster much lower than premium technology or product-like assets.

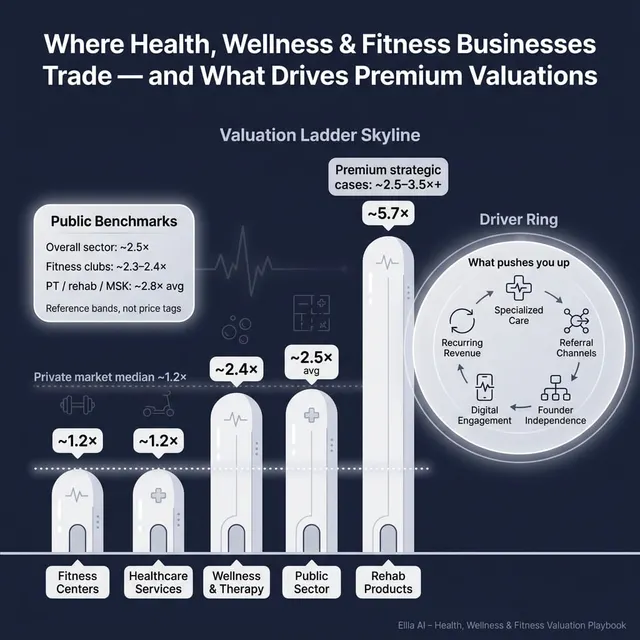

Across the precedent transactions, the overall average EV/Revenue multiple is about 2.6x, but the median is only about 1.2x. That gap matters. It tells you that a few higher-multiple deals can pull the average upward, while many real-world service businesses transact closer to the lower end.

For health, wellness, and therapeutic service providers, the average and median revenue multiple are both about 2.4x, with EBITDA multiples around 4.0x where disclosed. Fitness center and gym-based wellness services are around 1.2x revenue. Healthcare services providers are also around 1.2x revenue, though EBITDA multiples can be higher when earnings quality is strong. Rehabilitation and mobility health products show a much higher revenue multiple, around 5.7x, but that category is more product-oriented and less relevant for a local clinic or gym-based service business.

For founders, the main takeaway is simple: private market buyers tend to be disciplined. They may pay strategic prices for scarce capabilities, but they will not usually pay software-like multiples for a local, people-intensive service business.

Scale helps, but scale alone is not enough. A large gym network or clinic footprint can be valuable, yet the data suggests that distributed physical infrastructure by itself does not always create premium multiples. The premium comes when scale is paired with specialization, strong margins, repeatable growth, digital engagement, or strategic fit.

4.2 Public Companies

Public markets give useful reference points, but they are not direct price tags for private businesses. Public companies are usually larger, more diversified, more liquid, and better known to investors. Smaller private companies usually trade at a discount unless they have very strong strategic value.

As of mid to end 2025, the public company data shows an overall average EV/Revenue multiple of about 2.5x and a median of about 1.8x. Overall EV/EBITDA averages about 13.6x, with a median around 7.9x. Fitness club and gym operators trade around 2.3x to 2.4x revenue and about 6.1x EBITDA on average and median. Physical therapy, rehabilitation, and MSK or pain care providers show an average revenue multiple around 2.8x, but the median is only about 1.1x, which again shows how much the higher-end assets can skew the average.

Public companies with larger networks, faster growth, stronger margins, and clear rollout potential tend to trade better. More mature, lower-margin, slower-growth, or heavily labor-dependent groups tend to trade lower.

For a founder, public multiples should be used as reference bands, not direct valuation formulas. A smaller private business may trade below public peers because it has less scale, less liquidity, more customer concentration, weaker systems, or more founder dependence.

There are exceptions. A scarce asset with strong clinical specialization, strong margins, high growth, or a perfect strategic fit can sometimes trade above where a simple public-comp comparison would suggest. But that premium has to be earned through evidence.

5. What Drives High Valuations - Premium Valuation Drivers

High valuations come from reducing buyer risk and increasing buyer excitement. In this sector, the strongest premium drivers are not vague wellness language. They are practical, provable features that make the business more strategic, more scalable, or more defensible.

Specialized Clinical or Therapeutic Positioning

Buyers pay more when a business is not just “wellness” but solves a specific problem. Examples include chronic pain, musculoskeletal care, neurological rehabilitation, occupational health, senior mobility, women’s health, sports recovery, and post-surgery rehabilitation.

Specialization matters because it gives buyers a clearer reason to own the business. A specialist care pathway can plug into hospitals, employers, insurers, national health platforms, or larger therapy networks. A general wellness center is easier to replace.

Strategic Fit for the Buyer

Some businesses are valuable because they change what the buyer can offer. A gym platform may want physiotherapy. A healthcare group may want employer wellness. A rehabilitation company may want specialized mobility products. A consumer health brand may want digital coaching or remote care.

This is where valuation can stretch. Buyers pay more when your business helps them enter a new category, cross-sell into an existing customer base, or strengthen a strategic gap they cannot easily build themselves.

Scalable Delivery Infrastructure

Multi-site reach, local density, employer channels, referral networks, and standardized operations can all improve valuation. Buyers like businesses that can be expanded without reinventing the model at every location.

But scale by itself is not enough. A large footprint with weak margins and high churn is not a premium asset. A smaller platform with repeatable economics, strong local density, and a clear rollout plan can be more attractive.

Technology-Enabled Care or Engagement

Digital tools can help a physical services business become more scalable. This does not mean you need to become a software company. It can mean online coaching, remote follow-ups, digital exercise plans, member apps, patient engagement tools, scheduling automation, outcomes tracking, or hybrid in-person and virtual programs.

Buyers care because digital engagement can improve retention, reduce no-shows, extend care beyond the physical site, and create more touchpoints with customers.

Strong Profitability and Earnings Quality

Revenue is important, but buyers ultimately care about how much cash the business can produce. Strong EBITDA margins, consistent monthly performance, low customer acquisition costs, and predictable revenue all support higher valuation.

Earnings quality means buyers trust the profit. Clean accounting, clear add-backs, sensible owner compensation, and accurate location-level reporting make your numbers easier to believe.

Recurring Revenue and Customer Stickiness

Memberships, treatment packages, employer contracts, subscriptions, long-term referral relationships, and recurring care plans are valuable because they make revenue easier to forecast.

A buyer will pay more for revenue that is likely to repeat next month and next year. They will pay less for revenue that must be resold every day.

Management Depth and Founder Independence

A business that depends entirely on the founder is harder to buy. Buyers want to know that the team can keep operating after closing.

A strong general manager, clinical director, head of operations, finance lead, or location managers can increase confidence. Even if you stay for a transition period, the buyer wants to see that the business is not built only around your personal relationships.

6. Discount Drivers - What Lowers Multiples

Some businesses look strong on the surface but receive lower offers once buyers study the details. The most common issue is that revenue is less predictable than it first appears.

High churn is a major discount driver. For fitness businesses, buyers will study membership cancellations, freezes, promotional sign-ups, and how long members actually stay. For therapy and rehab businesses, they will look at treatment completion, repeat visits, referral quality, and no-show rates.

Another discount driver is a people-intensive model with weak margins. If revenue growth requires hiring more staff at the same rate, and each location has limited capacity, buyers will treat growth as slower and more expensive. Labor shortages, clinician turnover, trainer churn, and wage inflation all matter.

A weak or unclear service mix can also hurt valuation. If your business says it is a wellness, fitness, therapy, rehab, and consulting platform all at once, buyers may struggle to understand what they are buying. Broad can be attractive, but only if it is organized into a clear model.

Other discount drivers include:

In the source data, lower multiples are often attached to more conventional service businesses, smaller providers, or models where growth remains tied to physical sites and staff. Higher outcomes tend to require something extra: specialization, digital extension, strong earnings, or strategic scarcity.

The good news is that many discount drivers can be improved in 6-12 months. You may not be able to become a national platform overnight, but you can clean up reporting, reduce churn, improve margins, document referral sources, and make the business easier to diligence.

7. Valuation Example: A Health, Wellness & Fitness Services Company

Let’s use a fictional company called VitalPath Wellness & Rehab. The company and revenue level are fictional. This is not investment advice, not a formal valuation, and not a fairness opinion. It is a simple example to show how buyers may think.

Assume VitalPath has USD 10m of annual revenue. It operates two local facilities that combine fitness memberships, physiotherapy, rehabilitation programs, and health coaching. It has a strong local brand, but limited digital delivery, no proprietary technology, and growth still depends heavily on staff, space, and local demand.

The starting point is to select relevant comparables. Public fitness operators trade around 2.3x to 2.4x revenue on average and median, but many are much larger platforms. Public physical therapy and rehabilitation companies show a wide range, with a median closer to 1.1x revenue. Private fitness and healthcare services transactions in the data sit around 1.2x revenue for relevant service-heavy models.

That suggests a core range for a local, physical, people-intensive business should be lower than scaled chains, digital health platforms, or product-oriented rehab assets. For VitalPath, a base valuation range of roughly 0.9x to 1.4x revenue is defensible. On USD 10m of revenue, that implies USD 9m to USD 14m of enterprise value.

However, the range can move. If VitalPath had stronger premium drivers - such as a multi-site rollout model, employer contracts, specialized rehab pathways, strong EBITDA margins, low churn, digital patient engagement, and a deep management team - buyers might underwrite a higher multiple. If it had weak margins, messy financials, high churn, founder dependence, or no clear specialization, buyers might move lower.

The lesson is that two businesses with the same USD 10m revenue can be worth very different amounts. One may be a local service business with limited transferability. Another may be a scalable, specialized, high-retention care platform that multiple strategic buyers want.

Your job before a sale is to move the buyer’s view from “nice local business” toward “strategic, repeatable, and hard to replace.”

8. Where Your Business Might Fit - Self-Assessment Framework

Use this framework as a rough guide. It will not replace a valuation, but it will help you think like a buyer.

Score each factor from 0 to 2:

- 0 = weak or not proven

- 1 = acceptable but not exceptional

- 2 = strong and well documented

A high score means you are more likely to attract premium interest, especially if several buyers can see strategic value. A middle score suggests you may be in a fair market range, where process quality and buyer selection matter a lot. A low score does not mean you cannot sell, but it likely means you should fix the biggest issues before going to market.

Be honest with yourself. Buyers will find the weak spots anyway. The goal is not to pretend every metric is perfect. The goal is to know which improvements can have the biggest valuation payoff before you launch a sale process.

9. Common Mistakes That Could Reduce Valuation

The first mistake is rushing the sale. Many founders start speaking to buyers before their numbers, story, and process are ready. That usually leads to weaker offers because buyers see uncertainty and use it to negotiate.

The second mistake is hiding problems. If churn is high, if a key clinician is leaving, if a location is underperforming, or if revenue recognition is messy, the issue will usually surface during due diligence. Hiding problems destroys trust and can lead to price cuts, tougher deal terms, or a failed process.

Weak financial records are another major problem. Buyers want to see clean monthly profit and loss statements, revenue by service line, location-level profitability, payroll detail, add-backs, member or patient metrics, and clear EBITDA. If your financials are messy, buyers will assume risk even when the underlying business is strong.

A fourth mistake is not running a structured, competitive process. Research and market experience show that a well-run sale process with an advisor can lead to meaningfully higher purchase prices, often around 25% higher, because buyers know they are competing. A single-buyer conversation rarely creates the same tension.

Another common mistake is telling buyers the price you want too early. If you say you are looking for USD 10m, buyers may come back with USD 10.1m or USD 10.2m. That kills price discovery. In a proper process, you let the market show what the business is worth.

Industry-specific mistakes include overclaiming “platform” status without proof. A business is not a platform just because it has more than one service line. Buyers want evidence of repeatable growth, systems, management, and economics. Another mistake is presenting broad wellness language without clear differentiation. “Holistic” and “approachable” are nice, but they do not replace hard evidence of retention, specialization, outcomes, and profitability.

10. What Health, Wellness & Fitness Services Founders Can Do in 6-12 Months to Increase Valuation

Improve the Numbers

Start with financial clarity. Prepare clean monthly financials, separate revenue by service line, track gross margin, and show EBITDA clearly. If you have multiple locations, produce location-level reporting.

Review pricing. Many founders underprice memberships, therapy packages, coaching, or corporate wellness programs. Thoughtful price increases can improve margins without damaging retention if the value is clear.

Reduce avoidable leakage. Look at no-shows, underused staff hours, low-margin services, discounting, rent burden, and poor scheduling. Small improvements can materially increase EBITDA.

Strengthen Retention and Repeatability

Buyers pay more for revenue that sticks. Track member retention, patient repeat visits, package renewals, employer contract renewal, referral conversion, and treatment completion.

Build programs instead of one-off services. For example, a 12-week back pain rehabilitation program, senior mobility pathway, post-surgery recovery package, or employer wellness plan is often easier to sell, track, and repeat than ad hoc sessions.

Document why customers stay. Buyers want evidence that your retention is not accidental.

Make the Business Less Founder-Dependent

Build a second layer of leadership. Identify who runs operations, clinical quality, sales, finance, and customer experience when you are not there.

Document key processes. This includes onboarding, scheduling, member sales, referral management, treatment protocols, compliance, payroll, local marketing, and monthly reporting.

If buyers believe the business will weaken after you leave, they will discount the valuation or demand more earnout.

Sharpen the Strategic Story

Decide what you are really selling. Are you a local premium fitness brand, an integrated gym plus physiotherapy model, a rehabilitation platform, an employer wellness provider, or a specialist care network?

Then support that story with data. If you claim specialization, show outcomes, referral sources, clinician credentials, and patient retention. If you claim scalability, show site economics and a playbook for new locations.

Add Digital or Remote Engagement Where It Fits

You do not need to build a full technology company. But you can add remote follow-ups, digital exercise plans, app-based member engagement, online coaching, automated reminders, or outcomes tracking.

These tools can improve retention and show buyers that growth is not limited entirely to physical capacity.

11. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor can help you reach a broader and more relevant buyer universe. Instead of relying only on the obvious acquirers, AI can screen hundreds of potential buyers based on deal history, strategic fit, financial capacity, geography, and synergy signals. More relevant buyers usually means more competition, stronger offers, and a higher chance the deal closes if one buyer drops out.

AI can also speed up the process. Buyer matching, outreach preparation, marketing materials, financial analysis, and due diligence support can be done faster when expert advisors use AI properly. That can help founders reach initial conversations and offers in under 6 weeks in the right situations.

The human advisor still matters. The best outcomes come from expert M&A advisors who know how to frame the business, defend the numbers, manage buyer tension, and negotiate deal terms. AI improves speed and coverage, while experienced advisors provide judgment, credibility, and deal control.

Eilla AI combines expert M&A advisory with AI-native execution: broader buyer reach, faster preparation, sharper positioning, and Wall Street-grade process quality without traditional bulge bracket costs. If you’d like to understand how our AI-native process can support your exit, book a demo with one of our expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.