The Complete Valuation Playbook for Maritime Software Businesses

A practical guide to how maritime software businesses are valued and what drives high multiples.

If you are building a maritime software business and thinking about a sale in the next 1-12 months, valuation is probably on your mind. The market is active, but selective. Buyers still want digital tools that improve vessel operations, compliance, tracking, connectivity, safety, and logistics visibility - but they are much more careful about growth quality, profitability, and whether the product is truly mission-critical.

This playbook shows what maritime software businesses actually sell for, what public markets suggest as a reference point, why some companies earn premium multiples, and why others trade at the low end. It also gives you a practical self-assessment and a 6-12 month action plan to improve your position before going to market.

The ranges in this article are illustrative. They are not investment advice, a formal valuation, or a fairness opinion. Actual outcomes depend on your growth, margins, customer base, revenue quality, buyer appetite, and sale process.

1. What Makes Maritime Software Unique

Maritime software sits at the intersection of shipping, logistics, compliance, connectivity, data, and physical operations. That makes it different from a generic software business.

A normal software buyer may ask, “How fast is it growing?” A maritime software buyer will also ask, “Is this product embedded in vessel operations? Does it support regulatory compliance? Does it reduce downtime? Does it help customers manage risk at sea, across ports, or across cargo movements?”

The main types of companies in maritime software include:

The best businesses in this sector often combine three things: hard-to-replace workflows, recurring revenue, and data that becomes more valuable over time. If your platform is used every day to manage risk, meet regulatory needs, move cargo, or keep vessels connected, buyers will view you very differently than a business selling one-off projects or hardware.

The key risks buyers will always check are also sector-specific. They will test how much of your revenue is truly software versus services, whether revenue depends on hardware resale, whether customers are concentrated in a few fleets or regions, whether your data sources are defensible, and whether your product is required or simply “nice to have.”

2. What Buyers Look For in a Maritime Software Business

Buyers start with the basics: revenue scale, growth, gross margin, profitability, customer retention, and the quality of your financial records. But in maritime software, those basics are only the starting point.

They will also look closely at where your product sits in the customer’s daily operations. A tool used occasionally for reporting is less valuable than a platform that supports live vessel decisions, compliance checks, cargo visibility, cyber protection, or connectivity. The closer you are to a mission-critical workflow, the easier it is for buyers to believe your revenue will last.

Buyers also care about revenue type. Recurring subscription revenue is usually valued more highly than implementation revenue, consulting revenue, hardware resale, or project-based revenue. A business with USD 10m of mostly recurring software revenue can be worth much more than a business with the same revenue but heavy services, hardware, or low-margin project work.

Strategic buyers often ask: “Can we sell this into our existing customers?” If your software can be added to a larger logistics, satcom, marine equipment, fleet management, risk intelligence, or trade platform, you may be worth more to that buyer than you are on a standalone basis.

How private equity buyers think

Private equity buyers think in terms of entry price, improvement plan, and exit price. In plain English: they ask what they have to pay today, what they can improve over 3-7 years, and who might buy the company from them later.

They will look for levers such as price increases, better packaging, cross-selling into existing accounts, reducing churn, improving gross margin, and adding smaller acquisitions. They will also ask whether a larger strategic buyer, a larger private equity fund, or possibly public markets could value the company at a higher multiple in the future.

For a maritime software founder, this means the buyer is not only valuing what you are today. They are valuing what they believe the business can become under their ownership. The clearer that path is, the stronger your valuation case becomes.

3. Deep Dive: Software-Like Revenue vs Hardware or Project Revenue

The biggest valuation question in maritime software is simple: are you really a software business, or are you a maritime services, hardware, or project business with some software attached?

This matters because the data shows a wide gap between software-like maritime assets and equipment-heavy or services-heavy businesses. In the precedent transactions, some maritime connectivity, tracking, and operational software assets reached much stronger EBITDA multiples, while equipment and technical services assets often traded at much lower revenue multiples. The main reason is business model quality.

Buyers pay more for revenue that can scale without the cost base scaling at the same pace. If you sell another software subscription to another vessel, fleet, port, or logistics customer, your cost to serve that customer may be relatively low. But if each new dollar of revenue requires hardware procurement, installation teams, custom engineering, or project delivery, buyers will apply a lower multiple.

This does not mean hardware or services are bad. In maritime, they are often necessary. Connectivity may need devices. Vessel systems may need installation. Compliance platforms may need expert onboarding. The issue is whether those elements support a high-margin recurring software relationship, or whether they dominate the economics.

If your business looks more like the left column today, you do not need to change everything in 6 months. But you can improve the valuation story by separating revenue lines clearly, showing the gross margin of each line, packaging services as onboarding rather than core revenue, and proving that customers renew because the software is essential.

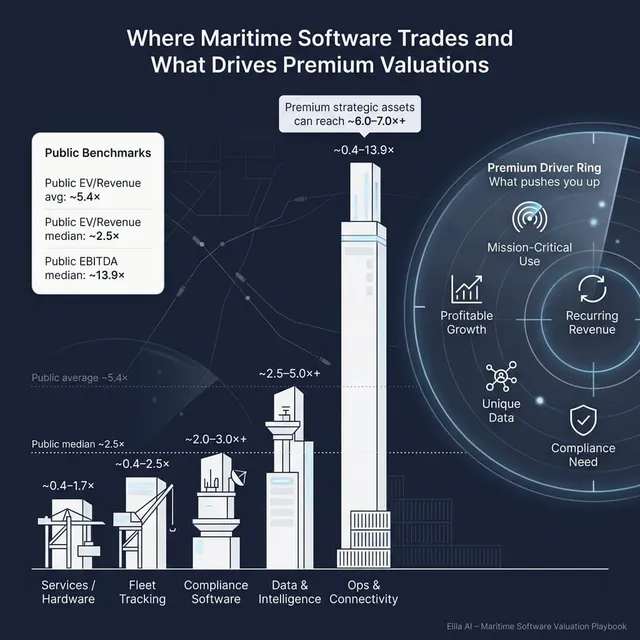

4. What Maritime Software Businesses Sell For - and What Public Markets Show

The valuation data shows a very wide range. That is normal in maritime software because the category includes high-margin data platforms, fleet telematics, satellite connectivity, maritime surveillance, logistics platforms, ship design technology, and services-heavy marine businesses.

The most important point for founders is this: headline averages can mislead you. A software business with recurring revenue, high gross margin, and strong retention should not be valued like a marine equipment company. But a loss-making, subscale software business should also not automatically expect the same valuation as a large public data platform.

4.1 Private Market Deals - Similar Acquisitions

The precedent transaction data shows an overall average EV/Revenue multiple of about 2.8x and a median of about 0.4x. The overall average EV/EBITDA multiple is about 10.4x, with a median of about 9.7x.

That wide gap between average and median tells you the market is not applying one simple rule. Some assets trade at very low revenue multiples because they are equipment-heavy, services-heavy, low-margin, or slower growth. Others trade at stronger EBITDA multiples because they are profitable, recurring, embedded in customer workflows, or strategically valuable to the buyer.

The private deal data suggests that maritime software businesses with strong margins, recurring revenue, and mission-critical connectivity or compliance positioning can attract premium interest. But the same data also shows that compliance alone is not enough. If the business model is low-margin or equipment-heavy, the valuation can still land near the bottom of the range.

4.2 Public Companies

Public market multiples provide useful reference points, but they are not direct price tags for private companies. Public companies are often larger, more liquid, more diversified, and better known to investors. They may also have stronger reporting, more predictable earnings, and access to cheaper capital.

Across the public comparable set, the overall average EV/Revenue multiple is about 5.4x and the median is about 2.5x. The overall average EV/EBITDA multiple is about 19.4x and the median is about 13.9x. These public market reference points are as of the mid to end of 2025 period reflected in the source data.

The highest public revenue multiples tend to appear in businesses with scale, scarce data, strong growth, mission-critical workflows, or platform characteristics. But several public companies with lower margins, hardware exposure, or slower growth trade much lower.

For founders, public multiples should be used as a reference band. A smaller private company is usually discounted for lower scale, lower liquidity, customer concentration, and execution risk. But a scarce, fast-growing, high-margin maritime software asset can still attract strong strategic interest if buyers believe the asset gives them something hard to build themselves.

5. What Drives High Valuations - Premium Valuation Drivers

Premium valuations usually come from a combination of factors. One strong feature helps, but buyers pay the most when several premium drivers appear together.

Regulatory and compliance relevance

Compliance-linked products often receive stronger buyer interest because they are less optional. In maritime, this can include sanctions screening, emissions reporting, safety workflows, cyber controls, voyage compliance, crew and vessel documentation, ballast water regulation, and trade-related checks.

Buyers like products that help customers avoid fines, delays, detentions, reputational damage, or operational disruption. If your software sits inside a required workflow, customers are less likely to cancel it when budgets tighten.

The key is proving that compliance is not just a feature. Buyers want to see that it drives renewals, supports pricing power, and makes your platform harder to replace.

Scalable software economics

The strongest valuation lens in the data is the difference between scalable software and hardware or project-heavy revenue. High gross margins tell buyers that each additional customer or vessel can add meaningful profit over time.

Practical examples include subscription modules, data feeds, compliance alerts, risk scoring, workflow automation, and customer dashboards that can be sold repeatedly without heavy customization.

If your business still includes hardware or services, show the split clearly. Buyers may still value the software revenue highly if they can see that the hardware and services are supporting the platform rather than dominating it.

Mission-critical connectivity and intelligence

Products that keep vessels connected, secure, visible, and compliant can become operational infrastructure. This is especially true when downtime, cyber risk, cargo disruption, or loss of visibility creates real financial consequences for the customer.

Buyers pay more when the product is embedded in daily operations. A platform that customers log into every day, integrate into other systems, and use to make live decisions will usually be more attractive than a reporting tool used once a month.

Growth with profitability

Growth is important, but the data shows that growth alone is not enough. Buyers prefer growth that comes with improving margins, strong retention, and a clear path to EBITDA.

A company growing 20 percent with improving gross margin and a path to profitability may be valued more confidently than a company growing faster but burning more cash every year. Buyers want to know whether growth is creating value or just consuming capital.

Integration-ready workflows

Strategic buyers pay more when your product can be plugged into their broader platform. This can mean integrations with fleet systems, ERPs, transport management systems, satellite networks, port systems, insurance workflows, banking compliance tools, or trade documentation platforms.

The more your product connects to other systems, the more useful it becomes to a buyer with a large customer base. Integration-ready assets are easier to cross-sell and easier to position as part of a larger platform.

Network reach and customer footprint

Maritime is a relationship-driven and networked industry. Buyers care about how many vessels, fleets, ports, cargo owners, insurers, or financial institutions you reach.

A broad installed base can make your business more strategic. It gives buyers a channel for cross-selling, a data advantage, and a stronger reason to acquire rather than build.

Clean execution and buyer confidence

Some premium drivers are not sector-specific, but they matter a lot. Clean financials, clear revenue recognition, low churn, diversified customers, a strong leadership team, and a credible forecast can all improve valuation.

Buyers pay more when they trust the numbers and believe the business can keep performing after the founder steps back.

6. Discount Drivers - What Lowers Multiples

Discounts usually come from risk. The more risk buyers see, the more they lower the multiple or structure the deal with earnouts, deferred payments, or other protections.

The most common discount driver in maritime software is a weak software story. If revenue is mostly hardware, installation, bespoke development, or consulting, buyers will not apply premium software multiples. They may still like the business, but they will value it more like a marine services or equipment business.

Negative EBITDA is another major issue, especially if there is no clear path to profitability. Some buyers will accept losses if growth is strong and gross margin is high. But if losses are widening, growth is modest, and the company is not clearly scaling, buyers become cautious.

Other common discount drivers include:

Industry-specific risks also matter. Maritime buyers will check whether you depend on third-party data access, whether vessel connectivity is reliable, whether your product handles cybersecurity properly, whether your compliance logic is current, and whether your customer base is exposed to shipping cycles.

The good news is that many discount drivers can be improved before a sale. Even if you cannot fully fix them in 6-12 months, you can measure them, explain them, and show buyers a credible improvement plan.

7. Valuation Example: A Maritime Software Company

Let’s make this practical.

Assume a fictional company called HarborSignal. HarborSignal is a maritime compliance and vessel intelligence platform. It sells recurring subscriptions to shipowners, managers, insurers, and trade compliance teams. Its tools include vessel monitoring, sanctions and risk alerts, voyage compliance workflows, and reporting dashboards.

HarborSignal has fictional revenue of USD 10m. The company and revenue level are made up for illustration. The valuation ranges below are designed to show how the logic works, not to provide investment advice or a formal valuation.

Step 1: Select the right reference set

For HarborSignal, the best starting point is not marine equipment or broad logistics services. The better reference set is maritime intelligence, vessel tracking, compliance software, and connectivity-related software.

The public maritime intelligence and vessel operations group shows revenue multiples that often sit around the low-to-mid single digits, with some higher outcomes for stronger, more strategic assets. Broader data and decision intelligence platforms can trade higher, but those companies are often much larger, more profitable, and more diversified.

The private transaction data also supports a wide range. Maritime connectivity, tracking, and operational software deals range from low multiples for small or lower-quality assets to much stronger outcomes for profitable, mission-critical platforms.

Step 2: Narrow the core range

For a USD 10m maritime compliance and intelligence software company, a reasonable illustrative core revenue multiple range might be 2.5x-3.5x if the business has:

- Solid but not breakout growth

- Good gross margin

- Mostly recurring revenue

- Some compliance relevance

- Limited proof of EBITDA scale

- Some customer concentration or niche-market risk

That would imply a base valuation range of USD 25m-35m.

If HarborSignal has stronger evidence - high retention, 60 percent-plus gross margin, strong annual growth, embedded compliance workflows, low churn, diversified customers, and a clear path to profitability - buyers may stretch higher.

If the business has weak retention, negative margins, heavy services revenue, or poor financial reporting, the multiple could fall below the core range.

Step 3: Apply scenarios

A premium strategic case would require more than “we are in maritime software.” It would need strong proof that the platform is mission-critical, recurring, high-margin, growing, integrated into customer workflows, and strategically valuable to a specific buyer.

This is why two companies with the same USD 10m of revenue can be worth very different amounts. One may be a low-margin project business with some software. Another may be a high-margin compliance platform that customers cannot easily remove. The revenue number is the same. The buyer’s view of quality is not.

8. Where Your Business Might Fit - Self-Assessment Framework

Use this framework to place yourself roughly within the valuation spectrum. Score each factor from 0 to 2:

- 0 = weak or not proven

- 1 = acceptable but not exceptional

- 2 = strong and well evidenced

Be honest. The goal is not to make yourself feel good. The goal is to identify which improvements could create the biggest valuation lift before a sale.

How to interpret your score

This is not a formula. It is a practical way to think like a buyer. If you score low on a high-impact factor, fixing that may matter more than adding a small new feature or chasing a marginal customer.

9. Common Mistakes That Could Reduce Valuation

The first mistake is rushing the sale. Many founders go to market before their numbers, story, and process are ready. Buyers then find gaps, ask harder questions, and reduce their offers.

The second mistake is hiding problems. If churn is rising, a large customer is at risk, a data source is unstable, or a product module has issues, buyers will usually find out during due diligence. Hiding problems destroys trust. Explaining them clearly, with a plan, is almost always better.

Weak financial records are another major value killer. Buyers want to see clean revenue by product line, recurring versus non-recurring revenue, gross margin by revenue type, customer retention, churn, and EBITDA adjustments. If your records are messy, buyers may assume the business is riskier than it really is.

Founders also hurt valuation by not running a structured, competitive process. Research and market experience show that running a competitive sale process with an advisor typically leads to meaningfully higher purchase prices, often around 25 percent higher, because buyers know they have to compete.

Another common mistake is revealing the price you want too early. If you tell buyers you are looking for USD 10m in enterprise value, many will come back at USD 10.1m or USD 10.2m. You have killed price discovery. A better process lets the market show you what the business is worth to different buyers.

Industry-specific mistakes include failing to separate software revenue from hardware, installation, and services revenue. Another is overclaiming “compliance” without proving that customers actually buy, renew, and expand because of compliance needs.

10. What Maritime Software Founders Can Do in 6-12 Months to Increase Valuation

Improve the numbers buyers care about

Start by cleaning your revenue reporting. Break revenue into recurring software, usage-based data, services, hardware, implementation, and other categories. Show gross margin for each one.

Then focus on retention. Buyers care deeply about whether customers stay and pay more over time. Track logo retention, revenue retention, churn reasons, renewal timing, and expansion revenue. Even if the numbers are not perfect, showing control and understanding improves confidence.

If EBITDA is negative, build a credible path to profitability. You do not necessarily need to be highly profitable before sale, but buyers need to understand how the business can scale.

Strengthen the software story

Make it easy for buyers to see that you are a software or data platform, not just a services business. Package repeatable modules, reduce custom work, standardize implementation, and document how new customers are onboarded.

If you have hardware or services, do not hide them. Explain their role. Show whether they help acquire customers, enable recurring revenue, or support the platform.

Prove mission-critical use

Collect evidence that customers rely on your product. This can include daily usage, number of vessels monitored, alerts processed, compliance reports generated, integrations used, or time saved.

Customer stories matter, but metrics matter more. Buyers want proof that your product is embedded in operations and difficult to replace.

Reduce obvious risks

Address customer concentration where possible. Renew key contracts before launching a sale process. Tighten cybersecurity documentation. Review third-party data dependencies. Make sure compliance claims are accurate and current.

You may not be able to remove every risk. But you can reduce the fear around them by preparing clear explanations and evidence.

Prepare the buyer story

Build a clear narrative around why your company matters now. For maritime software, strong themes include regulation, sanctions and risk complexity, fleet digitalization, vessel connectivity, emissions pressure, cyber risk, and the need for better operational visibility.

The best story is not “we are a good business.” It is “we solve a painful and growing problem, our customers rely on us, and a buyer can make this bigger.”

11. How an AI-Native M&A Advisor Helps

An AI-native M&A advisor can improve outcomes by expanding the buyer universe. Instead of relying only on the obvious acquirers, AI can help identify hundreds of qualified buyers based on deal history, strategic fit, financial capacity, customer overlap, product gaps, and other signals. More relevant buyers usually means more competition, stronger offers, and a higher chance the deal closes if one buyer drops out.

AI can also speed up the early stages of a process. Buyer matching, outreach preparation, process marketing materials, and due diligence support can move faster when technology handles the research-heavy work. In many cases, this can help founders reach initial conversations and offers in under 6 weeks.

The best model is not AI replacing advisors. It is expert human M&A advisors using AI to do better work faster. Experienced advisors still drive positioning, negotiation, buyer credibility, process tension, and deal judgment. AI helps them prepare stronger materials, test more buyer angles, and support diligence with more speed and consistency.

For founders, the outcome is Wall Street-grade advisory quality without traditional bulge bracket costs. If you would like to understand how an AI-native process can support your exit, book a demo with one of Eilla AI’s expert M&A advisors.

Are you considering an exit?

Meet one of our M&A advisors and find out how our AI-native process can work for you.